Loan default in Nigeria triggers a chain of events most borrowers never see coming — penalty charges that compound silently, credit bureau records that follow you for years, and collection tactics that range from legal to outright illegal. This guide breaks down exactly what happens at each stage and — more importantly — what you can do about it right now.

It Started With One Missed Payment

It is 3am on a Tuesday. Your phone buzzes.

“URGENT: Your loan of ₦15,000 is overdue. Failure to pay within 24 hours will result in legal action, BVN blacklisting, and notification of your employer and all your contacts.”

You stare at the screen. Heart pounding. You already know you cannot pay — your salary still has not come in, the market was slow this week, and that ₦15,000 feels like it has grown teeth overnight.

You are not alone. The Central Bank of Nigeria reported over 30 million active digital loan accounts in Nigeria as of 2024, and industry observers estimate that a significant portion of borrowers have experienced at least one missed payment. Most of them had no idea what that message actually meant — what was a legal threat, what was a bluff, and what rights they had in that moment.

This guide gives you the full, honest picture: what loan default in Nigeria actually means legally, what lenders can and cannot do to you under Nigerian law, and the exact steps to take if you are already behind on a payment.

What “Loan Default” Actually Means in Nigerian Law

A loan default occurs when you fail to repay according to the contractual terms you agreed to. In Nigeria’s digital lending space, most apps define default as missing a payment by 1 to 7 days past the due date — though the exact trigger varies by lender and is often buried in terms and conditions most borrowers skip.

Two stages matter here:

- Technical default: One missed or late payment. The loan is still recoverable. Most licensed lenders begin communication at this stage and strongly prefer resolution over escalation.

- Full default: No repayment for 30 to 90 days or more. The lender has now classified your loan as non-performing under CBN guidelines — specifically the CBN’s Prudential Guidelines, which require financial institutions to classify loans delinquent beyond 90 days as “lost” on their books.

The consequences at each stage are meaningfully different. Acting during the technical default window gives you the most negotiating power and causes the least damage to your financial profile.

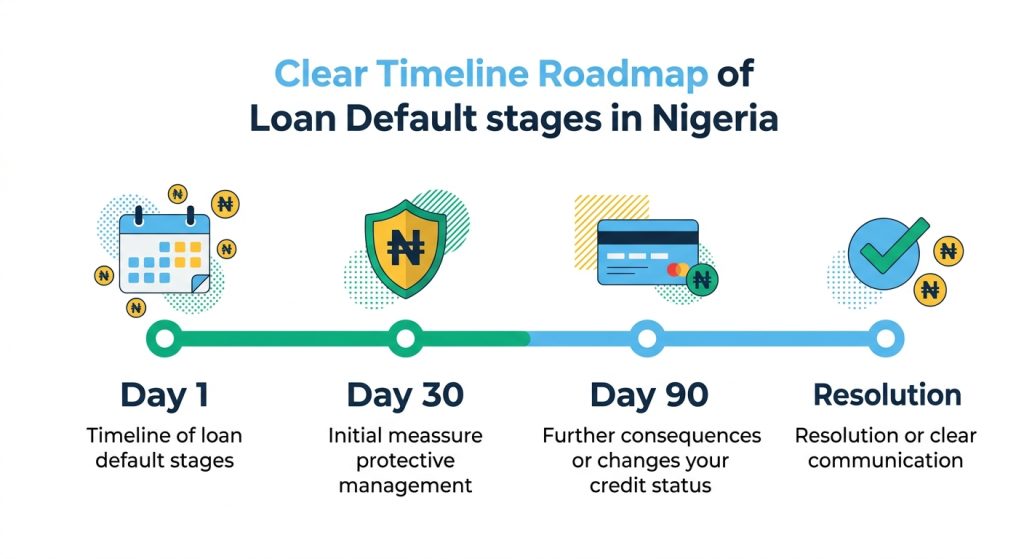

Day 1 to Day 30: What the First Month Actually Looks Like

The moment you miss your due date, a sequence begins. Here is what typically happens at licensed, regulated lenders in Nigeria:

Days 1–3: Automated SMS and in-app push notifications. Neutral to firm in tone. Sent every 24 to 48 hours.

Days 4–7: Direct phone calls begin — either automated voice calls or human agents. They will ask for a commitment date and may offer a short extension, especially if this is your first late payment.

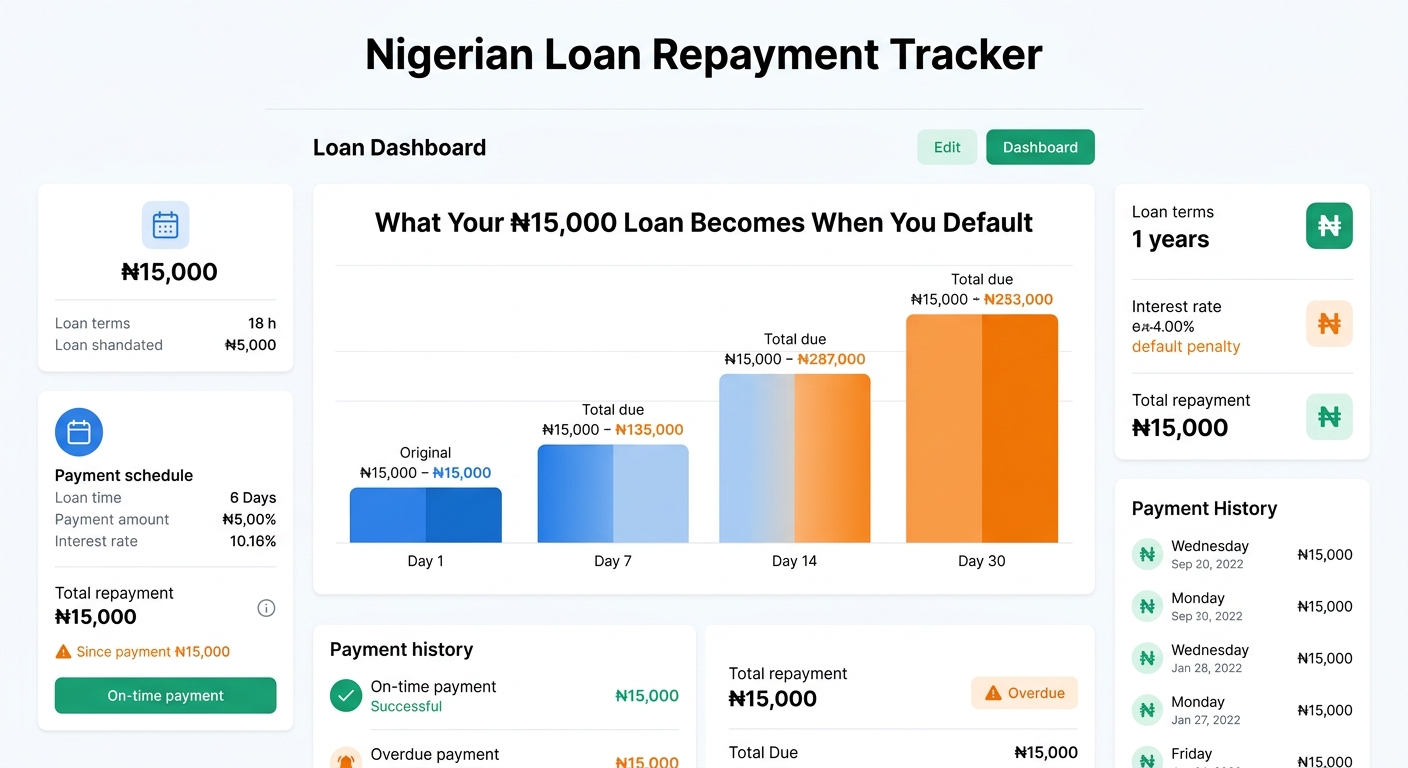

Days 7–14: Penalty interest and late fees start accumulating. This is the silent danger. A ₦15,000 loan with a daily penalty rate of 1% — common among digital lenders — becomes ₦15,150 after Day 1 of default. After 14 days, you owe ₦17,100. After 30 days, your balance can reach ₦19,500 — a 30% increase on the original principal without borrowing a single additional naira. Always check your loan agreement for the exact daily penalty rate.

Days 14–30: Escalated collection calls. More frequent, more urgent language. Some lenders begin explicitly mentioning credit bureau reporting at this stage.

The single most important advice for this window: Contact the lender before they contact you. A WhatsApp message, a call, an email — any proactive communication changes the dynamic entirely. Most CBN-licensed lenders have formal loan restructuring procedures precisely because defaulting borrowers are an expensive operational problem for them too. Silence is the worst possible strategy in this phase.

Day 31 to Day 90: When It Gets Serious

If a full month passes with no payment and no communication, the situation escalates materially.

Credit bureau reporting begins. Most CBN-licensed digital lenders are connected to at least one of Nigeria’s three licensed credit bureaus: CRC Credit Bureau, FirstCentral Credit Bureau, or CreditRegistry. After 30 to 60 days of delinquency, your loan status is reported as non-performing. This is not a rumour or a scare tactic — it is a standard regulatory requirement for licensed lenders under the CBN’s Credit Risk Management System (CRMS).

Third-party debt collection engagement. Some lenders refer accounts to external collection agencies at the 30 to 45-day mark. The tactics of these third-party agencies vary significantly in quality and legal compliance.

Internal blacklisting. The lender permanently flags your account. You cannot borrow from them again until the debt is fully resolved — and even then, re-approval is not guaranteed.

BVN flagging in the CRMS. Under the CBN’s Credit Risk Management System, lenders can report a defaulter’s Bank Verification Number to the centralised system. Other regulated lenders who run BVN checks during their credit assessment will see this flag immediately.

Your BVN and Credit Bureau Record: The Facts Without the Drama

There is more misinformation circulating about BVN blacklisting than almost any other topic in Nigerian personal finance. Here is what is factually accurate:

What a credit bureau record or CRMS flag DOES:

– Records your repayment history across all reporting lenders

– Flags your BVN as having a non-performing obligation

– Reduces your eligibility for bank loans, salary advance products, and regulated fintech credit

– Is visible to any lender who runs a formal credit check during their assessment process

– Can affect formal sector employment in financial services — some institutions run credit checks as part of background screening

What it does NOT do:

– It does not freeze your bank account or stop transactions

– It does not block your USSD transfers, airtime purchases, or POS payments

– It does not automatically notify your employer

– It is not permanent — negative marks can be removed once the debt is repaid and the lender updates the bureau (this typically takes 30 to 90 days after settlement)

You can check your own credit report for free once per year through the CRC Credit Bureau consumer portal or FirstCentral. Knowing exactly what is on your file is the first practical step in managing a loan default situation in Nigeria — you cannot fix what you have not seen.

5 Things Loan Apps CAN and CANNOT Legally Do to You

This section can save you from weeks of unnecessary fear. The Federal Competition and Consumer Protection Commission (FCCPC) issued its Limited Interim Regulatory/Registration Framework and Guidelines for Digital Lending in 2022, and these rules have real force — several apps have already lost their operating approvals for violations.

What licensed lenders CAN legally do:

- Charge penalty interest and fees that were disclosed in your original loan agreement

- Report your default to licensed credit bureaus

- Call you directly during reasonable hours (generally 8am to 9pm)

- Refer your debt to an FCCPC-compliant debt collection agency

- Pursue legal action to recover the outstanding balance through Magistrate Court or Small Claims Court

What NO lender can legally do under FCCPC digital lending guidelines:

- Call you before 8am or after 9pm in a harassing pattern

- Use threatening, abusive, or profane language in any communication

- Contact your family members, friends, colleagues, or employer without your explicit, informed prior consent

- Post your name, photo, or debt details in public forums, social media groups, or WhatsApp broadcast lists

- Send fake legal notices disguised as EFCC, police, or court correspondence

If a lender you are dealing with has done any of the above, you have grounds to file a formal complaint. The FCCPC accepts digital lending complaints through their official website and email channels. Document everything: screenshots, call logs, and message timestamps with dates.

The “We Will Call Your Contacts” Threat: A Direct Answer

This is the most psychologically damaging tactic in Nigerian digital lending, and it deserves a direct, unambiguous answer.

When you install most loan apps, you are prompted to grant access to your phone contacts during onboarding. Some lenders have used this access to systematically call borrowers’ employers, parents, spouses, and acquaintances to report outstanding debts — sometimes reading out exact loan amounts to humiliate borrowers into paying.

Is it legal? No. The FCCPC guidelines explicitly prohibit contacting third parties for debt collection purposes without clear, specific, informed consent. Granting contacts access during app installation does not constitute consent for debt collection harassment of those contacts.

Is it still happening? Unfortunately, yes — primarily among unregistered lenders and apps operating outside the FCCPC approval framework. This is precisely why verifying whether a lender is FCCPC-approved before downloading their app is not optional. It is the single most important due diligence step a borrower in Nigeria can take.

If a lender has called your contacts without consent: screenshot the evidence, file a complaint with the FCCPC, and stop using the app immediately.

Can They Actually Take You to Court? Real Numbers

Short answer: yes — but the economics determine how often it actually happens.

Most digital lenders operate in the ₦5,000 to ₦300,000 range. Filing a case at Magistrate Court or Small Claims Court in Nigeria involves filing fees and legal representation costs. For debts under ₦50,000, the cost of litigation typically exceeds the practical recovery value — which is why most lenders pursue collection through phone pressure rather than courtrooms.

For debts above ₦100,000, legal action is a realistic possibility. A court judgment against you can result in:

- Garnishee proceedings — the court orders your bank to release funds directly to the creditor

- Salary attachment orders — the court instructs your employer to deduct from your salary at source

- Asset attachment — in cases involving larger amounts, seizure of identifiable assets

The critical point: debt does not disappear by being ignored. The Limitation Law in most Nigerian states gives creditors a six-year window to pursue loan recovery in court. A ₦50,000 debt ignored for two years — with daily penalty interest still accumulating — can become a ₦200,000+ legal judgment. The mathematics are unambiguous.

If You Are Already Defaulting: Your 5-Step Recovery Plan

If you are reading this because you have already missed a payment, here is your action plan — in strict order of priority:

Step 1: Make contact today. Not tomorrow. A WhatsApp message, a call, or an email. Explain your situation factually. Silence is interpreted as refusal to pay — not inability to pay — and it triggers the most aggressive collection responses.

Step 2: Ask specifically for restructuring or an extension. Use these words: “I am experiencing a temporary cash flow problem and would like to discuss a revised repayment schedule.” Licensed lenders have internal processes for this. It is not begging — it is using the system as it was designed to be used.

Step 3: Make a partial payment if any amount is accessible. Even ₦2,000 toward a ₦20,000 balance demonstrates good faith, creates a documented payment record, and often pauses the most aggressive collection activity from compliant lenders.

Step 4: Calculate your actual current balance. Penalty rate × days overdue × outstanding principal = your real current debt. Knowing the exact number removes the fear of the unknown and allows you to prioritise this obligation correctly against your other expenses.

Step 5: Do not take a new high-interest loan to pay off a defaulted one without a clear calculation. Compare the new loan’s total cost against the daily penalty rate you are currently accumulating on the defaulted loan. Sometimes restructuring the original loan is mathematically better than taking on new debt. Run the actual numbers before deciding. Our guide on loan interest rates in Nigeria explains how to calculate the true cost comparison.

How to Never Default Again: Borrow Smarter From Today

The most expensive loan is always the one you cannot repay. These four structural rules protect you before you sign anything:

The 30% Rule: Never let a single loan repayment exceed 30% of your expected income for that period. If your salary is ₦80,000 and you borrow ₦60,000 due in 30 days, default is nearly mathematically certain. Limit your exposure before you sign.

Read the penalty clause first — not last. The daily penalty rate matters more than the headline interest rate for short-term digital loans. A loan advertised at “5% monthly interest” with a “1% daily default penalty” can quadruple in total cost within 60 days of default.

Set a repayment reminder 3 days before the due date. A significant share of loan defaults in Nigeria are not refusals to pay — they are failures to remember until it is too late. A free calendar reminder can save you thousands of naira in penalty charges.

Build a ₦10,000 to ₦20,000 emergency buffer in a separate account before taking any loan. This single habit eliminates the most common default trigger: a short-term cash gap between the loan due date and your salary payment date.

Frequently Asked Questions About Loan Default in Nigeria

Can a loan app share my data with other companies without my consent?

No. Under the Nigeria Data Protection Regulation (NDPR) and FCCPC guidelines, lenders cannot share your personal data — including your loan status — with third parties without explicit consent. Violations can be reported to the National Information Technology Development Agency (NITDA).

How long does a loan default stay on my credit report in Nigeria?

Negative credit information typically remains on Nigerian credit bureau files for up to seven years. However, once you repay the debt and the lender updates the bureau, the account status changes from “non-performing” to “settled” — a meaningfully different designation that future lenders will distinguish when reviewing your profile.

If I pay after defaulting, is my credit record immediately clean?

Not immediately. The lender must submit an update to the credit bureau, which can take 30 to 90 days to reflect on your file. You can follow up directly with the bureau after settlement to confirm the update has been processed correctly.

What if I genuinely cannot pay at all — no income, no assets?

Contact the lender and explain the situation in writing with documentation if possible. Many licensed lenders have hardship provisions for genuine cases. Nigeria does not have a formal personal bankruptcy regime equivalent to those in some other countries, but courts can be petitioned in extreme circumstances. For serious situations, seek advice from a qualified Nigerian legal practitioner.

The Honest Bottom Line

Loan default in Nigeria is serious — but it is not the end of your financial life, and it is absolutely not the uncontrollable disaster that 3am SMS messages are designed to make you believe it is.

The consequences are real: accelerating penalty charges, credit bureau records, escalating collection pressure, and in specific circumstances, legal action. But every single one of these consequences is manageable when you engage early rather than disappearing into silence.

You have rights under FCCPC guidelines. Harassment, public shaming, and contact-list attacks are illegal and reportable. The regulatory institutions exist specifically to protect you — but only if you use them.

The borrowers who suffer the worst outcomes from loan default in Nigeria are not the ones who cannot pay. They are the ones who panic, go silent, and let the debt compound in the dark while the lender’s legal options quietly expand. Face it early. Negotiate directly. Make partial payments. Document every interaction.

And when you are ready to borrow again, choose a lender that shows you every naira you will pay before you sign — not buried in fine print after the fact.

Looking for a loan that does not come with 3am threats? SmartLoans.ng connects you with regulated, FCCPC-compliant lenders who are transparent about every cost from the first screen. Check your options in under 2 minutes — no commitment, no hidden fees.