Your salary lands. Three days later, you’re wondering where it went. Here’s the system that fixes that — permanently.

You received your alert. ₦85,000. ₦120,000. ₦200,000. Whatever the number, it felt like enough when it hit.

Then the landlord called. Then your data finished. Then your child’s school sent that WhatsApp message. Then the fuel price jumped again. By the 18th of the month, you’re checking your balance and holding your breath.

This is not a willpower problem. This is a system problem — and every system problem has a system solution.

Understanding how to budget on a Nigerian salary is the most practical financial skill you can build right now. The 50/30/20 rule is one of the most battle-tested personal finance frameworks in the world — but most Nigerian versions are written for people earning ₦500,000 a month in Lagos Island apartments. This guide is not that.

This is the version for the teacher earning ₦65,000 in Kano. The corper on ₦77,000 allawee in Benue. The nurse earning ₦110,000 in Ibadan. The market trader’s wife on ₦45,000 household allowance in Aba. Real numbers. Real Nigerian life.

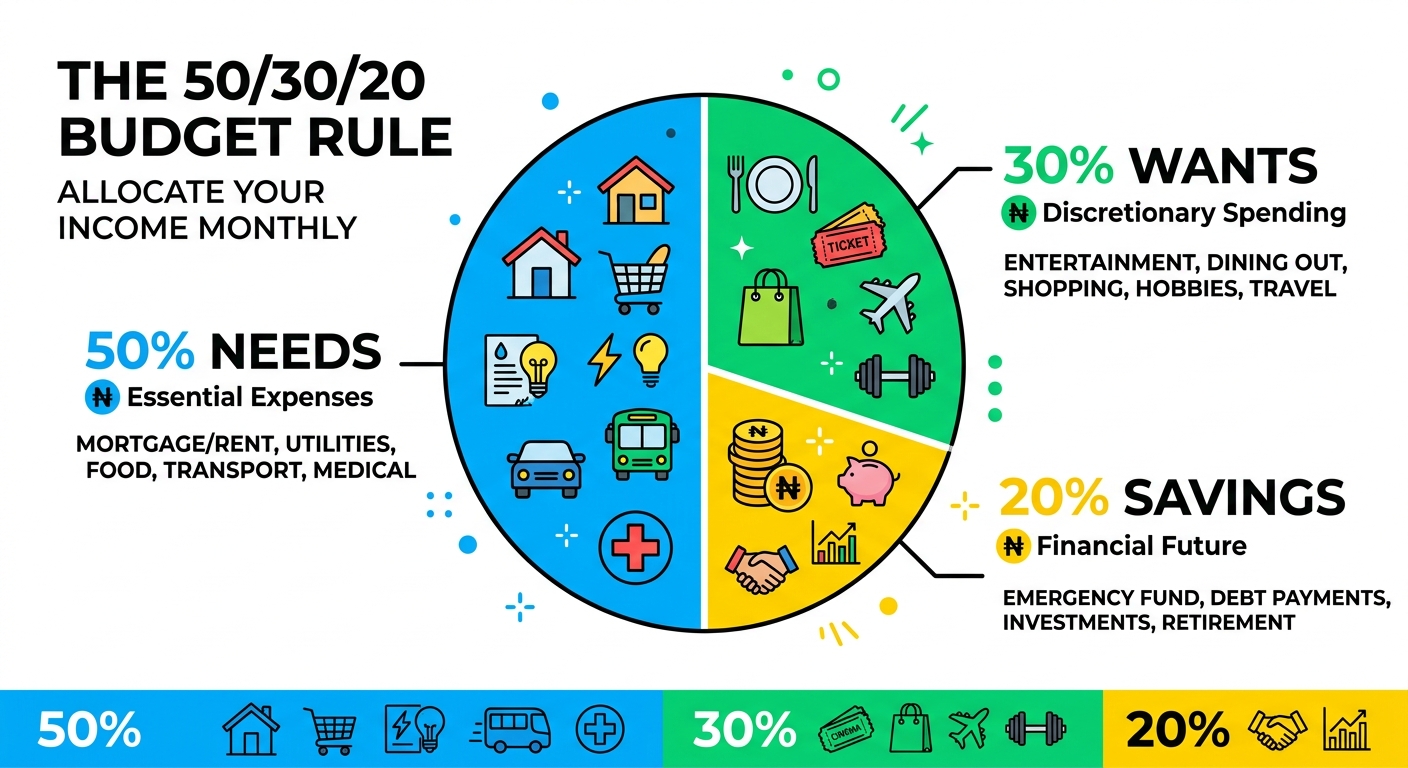

What the 50/30/20 Rule Actually Means

The rule was popularised by U.S. Senator Elizabeth Warren in her book All Your Worth, but the math works in any currency and any economy — including yours.

Here is the simple breakdown:

- 50% of your take-home pay → Needs (non-negotiable survival costs)

- 30% of your take-home pay → Wants (things that make life bearable, not just survivable)

- 20% of your take-home pay → Savings and debt repayment

That’s it. No spreadsheet degree required.

The genius of this rule is that it does not tell you what to cut — it tells you what percentage each category of your life deserves. You decide the details. For salary budgeting in Nigeria, the framework requires honest adaptation, which this guide walks through step by step.

According to the National Bureau of Statistics (NBS), Nigeria’s inflation rate remained above 30% through much of 2024 and into 2025, compressing real purchasing power for low- and middle-income earners. That context matters: the goal of this budget framework is not perfection — it is control inside a difficult environment.

Step 1 — Start With Your Real Take-Home Pay, Not Your Gross Salary

This is where many Nigerians go wrong from day one. Your gross salary is what your offer letter says. Your take-home is what actually lands in your account after PAYE tax, pension deduction (typically 8% employee contribution under Nigeria’s Contributory Pension Scheme governed by PenCom), and any cooperative or union deductions.

Real ₦ Example:

| Deduction | Amount |

|---|---|

| Gross salary | ₦120,000 |

| PAYE tax (estimated) | ₦8,000 |

| Pension deduction (8%) | ₦9,600 |

| Cooperative deduction | ₦5,000 |

| Real take-home | ₦97,400 |

Build your monthly budget in Nigeria on the number that actually enters your account. Everything else is fiction. Using your gross salary as a budgeting base is how people end up ₦15,000 short before the month even begins.

Step 2 — Map Your “Needs” (The 50% Bucket)

For a salary earner in Nigeria, needs typically include:

- Rent (calculated monthly, even if you pay annually)

- Food: market runs, cooking gas, water

- Transport: fuel, Bolt/InDriver, BRT card, okada money

- Electricity: NEPA prepaid token

- Data and basic phone airtime

- School fees installments

- Essential medications or health costs

Real example — ₦97,400 take-home:

| Expense | Monthly Cost |

|---|---|

| Rent (₦300,000/year ÷ 12) | ₦25,000 |

| Food & groceries | ₦18,000 |

| Transport | ₦7,000 |

| Electricity (NEPA token) | ₦5,000 |

| Data (2 lines) | ₦4,000 |

| Child’s school fees installment | ₦6,000 |

| Total Needs | ₦65,000 |

₦65,000 out of ₦97,400 = 66.7% — above the 50% target.

This is real Nigeria. The 50% rule will not fit perfectly for most low-income earners. The honest adaptation? Treat 50–65% as your acceptable needs range and focus your energy on keeping wants lean and savings consistent. Knowing this in advance prevents the guilt spiral that makes people abandon budgeting entirely.

Step 3 — Define Your “Wants” (The 30% Bucket) Honestly

Wants are the grey zone where most Nigerian budgets silently collapse.

Wants include:

– Eating out (suya, buka, Mr Biggs)

– Streaming subscriptions (Netflix, Showmax)

– New clothes or accessories beyond basic need

– Weekend outings, beer with colleagues

– Owambe contributions beyond your realistic means

– Hair, nails, grooming beyond basic care

Where this gets tricky in Nigerian culture:

Aso-ebi. Church and mosque donations above your set budget. “Small chops” money for family events. The pressure to appear okay when you are not. These social wants are real — they carry genuine social consequences — but they must be capped or they consume every naira left after needs.

Real example continued:

With ₦97,400 take-home and ₦65,000 already committed to needs, you have ₦32,400 remaining.

Strict 30% wants allocation = 30% × ₦97,400 = ₦29,220

That leaves: ₦32,400 − ₦29,220 = ₦3,180 for savings. Essentially nothing.

This is the math that explains why most Nigerian salary earners are always broke. When needs consume 60–70% of income, continuing to allocate 30% to wants makes saving mathematically impossible. The intelligent adaptation: flip the remaining split to 20% wants and 10% savings when needs are heavy. Getting the habit right matters more than hitting the original percentages perfectly.

Step 4 — The Savings and Debt Bucket (The 20% Goal)

This bucket does two jobs simultaneously:

- Emergency buffer — money you park somewhere you cannot easily touch (PiggyVest SafeLock, Cowrywise, ALAT savings wallet, or a separate account with no mobile app access)

- Debt repayment — clearing existing loans, BNPL balances, cooperative debt

Why this bucket is your protection against loan dependency:

When your NEPA token runs out on the 22nd and your salary arrives on the 27th, a ₦5,000 emergency buffer in a locked savings wallet means you solve it yourself. Without that buffer, you are on a loan app by midnight, paying 20–30% monthly interest on ₦5,000 you would have had if you had simply saved ₦500 per week. Over 12 months, that single habit — saving ₦500 weekly — creates a ₦26,000 emergency fund.

The minimum viable savings habit:

Even ₦1,000 per week — ₦4,000 per month — saved in a vault you cannot casually access, compounds into a meaningful buffer within 3 months. If you have existing loan repayments, treat them as mandatory as rent. Missing them damages your credit score, invites collection harassment, and traps you in an expensive debt loop that defeats the entire purpose of managing your salary in Nigeria more carefully.

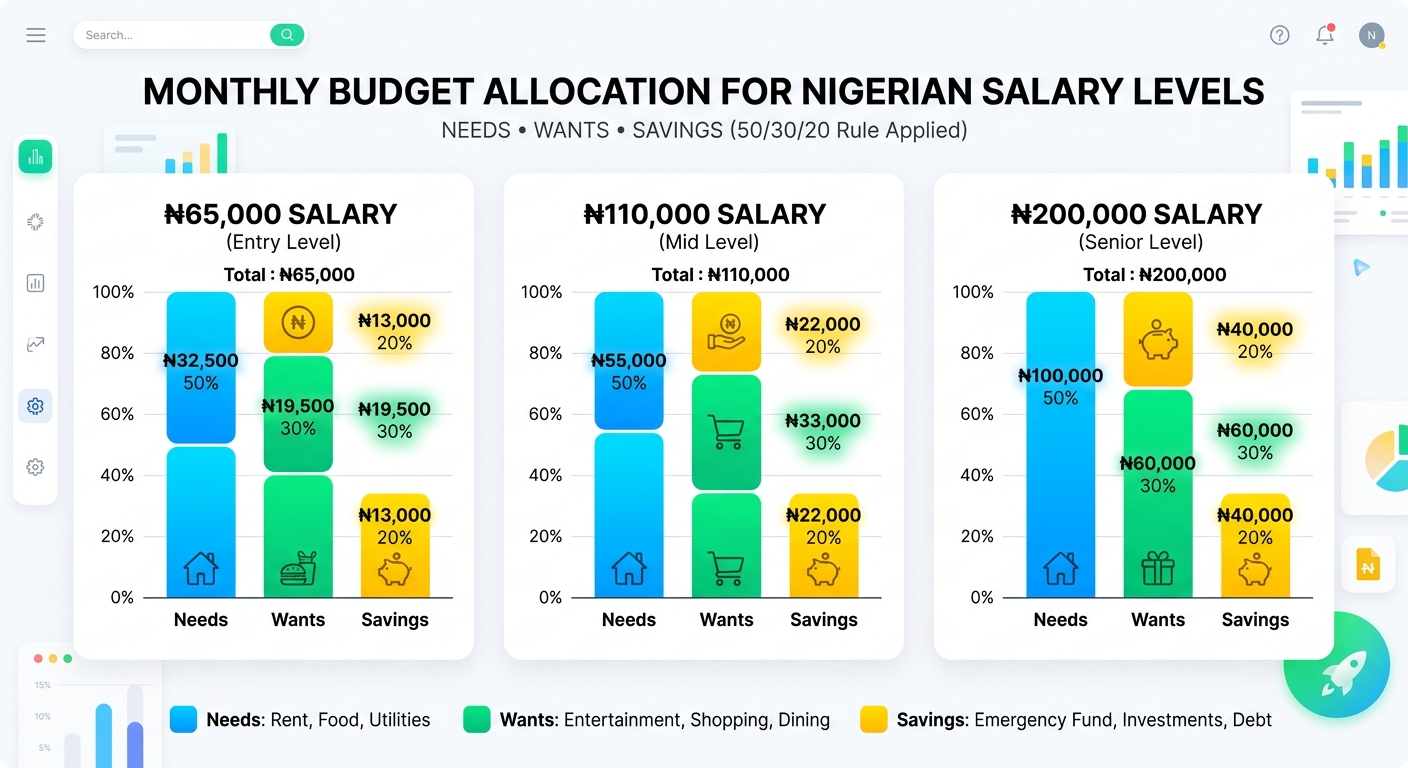

Step 5 — The Nigerian Budget Adaptation (Three Realistic Income Levels)

Here is what how to budget on a Nigerian salary actually looks like when adapted for real income levels across the country:

Scenario A — Take-home: ₦65,000 (teacher, civil servant, NYSC corper)

| Category | % | Amount |

|---|---|---|

| Needs (rent, food, transport, data, power) | 70% | ₦45,500 |

| Wants (social, personal care, occasional eating out) | 15% | ₦9,750 |

| Savings + loan repayment | 15% | ₦9,750 |

Scenario B — Take-home: ₦110,000 (nurse, mid-level private sector, accountant)

| Category | % | Amount |

|---|---|---|

| Needs | 60% | ₦66,000 |

| Wants | 20% | ₦22,000 |

| Savings + debt repayment | 20% | ₦22,000 |

Scenario C — Take-home: ₦200,000 (senior staff, Lagos private company)

| Category | % | Amount |

|---|---|---|

| Needs | 50% | ₦100,000 |

| Wants | 25% | ₦50,000 |

| Savings + investments | 25% | ₦50,000 |

The honest takeaway: the lower your income, the more needs consume your budget — and the more disciplined you must be with wants. This is not a moral failing. It is a structural economic reality in Nigeria, where the NBS reports that food inflation alone accounted for the largest share of CPI increases in 2024. The budget adapts to your reality. The habit of saving any amount still matters regardless of which scenario you fall into.

Step 6 — The “Salary Day Ritual” That Makes This Stick

A naira budget example on paper is theory. A salary day ritual turns it into practice.

On the day your salary lands, complete these steps — within the first 2 hours of receiving the alert:

- Transfer your savings first — before any expense. Even ₦2,000. Pay yourself first is the one non-negotiable discipline in every successful personal finance system worldwide.

- Clear any active loan repayment — protect your credit record before discretionary spending begins.

- Pre-load your needs — buy the month’s gas cylinder, load your NEPA token, pay the landlord if due. Lock these costs away before wants get a chance.

- Set a wants cash limit — withdraw or set aside a virtual “wants wallet” and stop when it is gone. No top-ups.

- Review weekly, not daily — obsessive daily balance-checking creates anxiety spending. A weekly 10-minute review is enough.

This ritual takes 30 minutes on salary day. It is the practical difference between surviving to month-end and opening a loan app on the 20th.

Step 7 — The 3 Budget Killers Specific to Nigerian Salary Earners

Budget Killer #1 — Ajo/Esusu Confusion

Thrift contribution (ajo, esusu, adashe) is savings — but only on the months you collect. The months you contribute without collecting, treat it as a fixed expense in your needs bucket. Many Nigerians double-count it as savings when the cash has already left their account.

Budget Killer #2 — Unbudgeted Family Remittances

If you regularly send money home to parents, siblings, or dependents — this is a need, not a want. Budget it as a fixed monthly line item. Pretending it will not happen every month is exactly why budgets collapse every month. Name it, fix the amount, and put it in the needs column.

Budget Killer #3 — Invisible Automatic Debits

DSTV, Showmax, iCloud storage, annual domain renewals, insurance premiums, Spotify — they debit silently. Pull your bank statement for the last 3 months and audit every automatic debit. Most people find at least two or three they had forgotten about. Cancel or consciously account for every single one.

Step 8 — When Budgeting Is Not Enough: The Right Way to Use a Loan

Even the most disciplined salary earner budget in Nigeria cannot absorb a ₦40,000 hospital emergency arriving without warning. Or a motorcycle breakdown that means zero income tomorrow. Or a landlord giving 48 hours’ notice.

Loans are not the enemy. Unplanned, panic-driven borrowing is.

When you need a loan despite having a budget:

- Borrow only the gap — not a round-number comfort amount. If you need ₦15,000, borrow ₦15,000, not ₦30,000.

- Understand the real cost — monthly interest of 15–25% on a ₦30,000 loan over 30 days means repaying ₦34,500–₦37,500. Know this before you sign, not after.

- Borrow from FCCPC-registered lenders only — verify on the FCCPC website or through the CBN’s licensed institutions list. Unregistered apps have no accountability for abusive collection practices.

- Build repayment into next month’s budget immediately — before spending a single naira of your next salary.

For transparent, FCCPC-compliant loan options without hidden fees, SmartLoans.ng is a resource worth reviewing before you borrow. And if you are already managing loan repayments alongside a tight budget, their guide on responsible borrowing in Nigeria offers practical frameworks for that specific situation.

Step 9 — The One Number That Changes Everything

Most Nigerians who want to learn how to budget on a Nigerian salary do not actually know their real monthly needs number. They do not know exactly what they spend on food. They guess. They estimate. They assume. They optimistically round down.

Track every single expense for 30 days. Every recharge card. Every keke fare. Every suya. Every time you “just” bought something small. Write it in a notes app. A paper jotter. Anywhere.

At the end of 30 days, you will see the truth. Based on patterns observed consistently in personal finance coaching across West Africa, most people discover they are spending 15–25% more than they estimated — entirely in small, invisible transactions that individually feel negligible.

That discovery alone — confronting the real number — is what finally makes a budget template for Nigeria stick. Not the spreadsheet. Not the app. The truth.

Step 10 — Inflation-Proofing Your Budget in 2026

Nigeria’s inflation environment requires one additional layer that classic 50/30/20 guides never mention: quarterly budget reviews.

Prices do not stay fixed. Cooking gas that cost ₦8,500 per 12.5kg cylinder in early 2024 crossed ₦14,000 in some markets by 2025. Tomatoes tripled. Data prices shifted. Transport fares moved with fuel costs.

Every three months, re-run your needs calculation from scratch. Do not assume last quarter’s numbers still apply. When you discover your needs have crept up — say, from 60% to 67% of take-home — make a conscious, immediate decision to cut wants proportionally rather than letting the savings bucket quietly drain to zero.

This quarterly recalibration is what separates people who maintain financial stability through inflation from people who wake up one day with no buffer and no plan. For anyone serious about how to budget on a Nigerian salary in 2026 specifically, this step is non-negotiable.

Conclusion: The Budget Is About Control, Not Deprivation

Nigeria is expensive. Inflation is real. Your salary has not kept up with the cost of living. None of that is your fault.

But every naira you earn still deserves a job — and giving it a job before it disappears is the single most powerful financial habit you can build right now, regardless of income level. How to budget on a Nigerian salary is not a question with a perfect answer. It is a practice you improve every month.

Start with your real take-home number. Separate needs from wants with brutal honesty. Save something — anything — on salary day before any other transaction. Review weekly. Recalibrate every quarter.

You will need to borrow less often. When you do need to borrow, you will borrow smarter, smaller, and with a clear repayment plan already written into next month’s budget.

For Nigerians looking for fast, transparent emergency loans with clear terms and no hidden charges, SmartLoans.ng provides access to FCCPC-compliant lenders — for those moments when life simply outspends even the best-prepared budget.

But first: build the budget. It costs nothing. It is the most valuable financial tool available to any Nigerian salary earner today.

Frequently Asked Questions

Q: Can I use the 50/30/20 rule if I earn below ₦60,000?

Yes, but you will likely run a 70/15/15 or even 75/10/15 split in reality. The principle stays the same — allocate deliberately, save first, keep wants honest. The percentages adapt to your reality.

Q: What counts as a “need” vs a “want” in Nigeria?

If life becomes genuinely dangerous, unhealthy, or unable to continue without it — it is a need. Data for job communication is a need. 20GB for Instagram is a want. The line is practical, not judgmental.

Q: How do I budget when my income is irregular (daily business, freelance, gig)?

Use your lowest income month from the past 6 months as your base. Anything above that goes 50% to savings, 50% to wants buffer. Irregular earners need a larger emergency fund — target 2 months of needs expenses minimum.

Q: Is ajo/esusu a substitute for savings?

Partially. It builds a lump sum — but lacks liquidity. Maintain a separate small emergency fund that you can access within 24 hours independently of your thrift group.