You Got Paid on the 25th. It’s the 10th. You Have ₦3,200 Left. You are not alone.

A survey by EFInA (Enhancing Financial Innovation and Access) found that over 60% of Nigerian adults report running out of money before their next income arrives. Not because they earn too little — though that is real — but because nobody ever sat them down and showed them what to do with money the moment it lands.

You get paid. Rent calls. Data finishes. The generator needs fuel. Someone in the family needs urgent help. Before you can breathe, the salary is half gone — and it is only the first week.

By the 20th, you are borrowing from colleagues. By the 25th, you are applying on a loan app just to buy food and transport until salary day.

Knowing how to stretch salary to month-end in Nigeria is not just a financial skill — it is survival arithmetic for millions of workers earning between ₦50,000 and ₦200,000 per month. This guide gives you a working system with real naira numbers, not generic advice copied from a Western personal finance blog.

Let us get into it.

Why Nigerian Salaries “Expire” Before Month-End

Before the fix, name the actual problem. Most Nigerians do not overspend because they are irresponsible. They overspend because of a specific, predictable set of conditions.

1. No plan on salary day. The money arrives as one large number. Without a system, it exits in random emotional chunks — rent pressure here, an urgent request there, celebration spending on the weekend.

2. Invisible micro-expenses. POS charges, airtime top-ups, a small “support” to a friend — each feels minor. Combined, they quietly consume ₦15,000–₦20,000 monthly without a single conscious decision.

3. Front-loaded spending. Most Nigerians spend heavily in the first two weeks after salary — catch-ups, stocking up, celebrations. Then they panic in the final ten days.

4. Zero buffer. When something unexpected happens — a broken phone, a medical bill, an emergency transport cost — there is nothing set aside. The only option becomes borrowing.

5. Social and cultural pressure. Owambe culture, aso-ebi obligations, family expectations — these are real Nigerian financial pressures that no Western budgeting framework was designed to handle. They must be part of any workable salary management strategy in Nigeria.

Understanding these root causes is step one. Now here is the system.

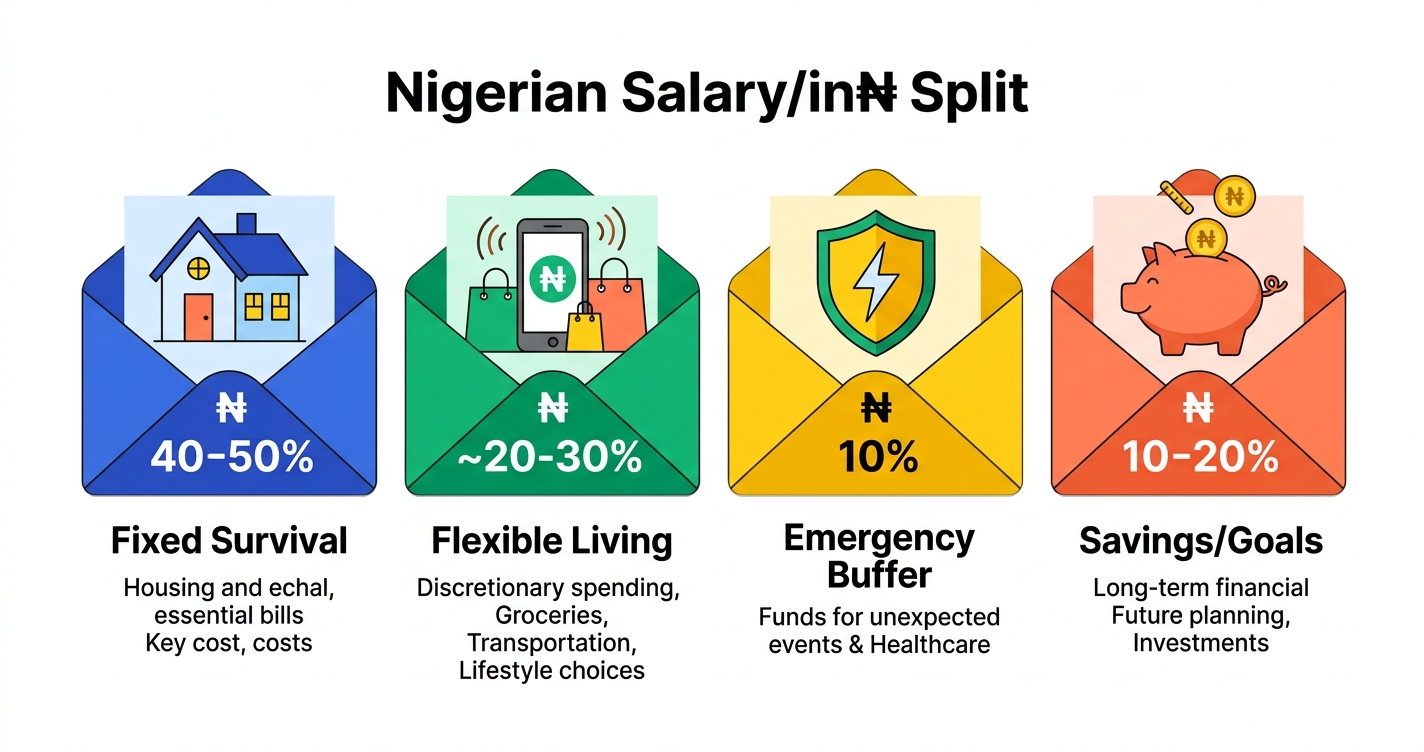

Step 1 — Divide Your Salary on Day 1: The 4-Part Split

The single most powerful thing you can do to stretch your salary to month-end in Nigeria is to stop treating your salary as one undivided amount.

The moment your salary arrives, split it into four categories — before you spend a single kobo. Here is how it works using a ₦80,000 monthly salary as a practical example:

| Category | % of Salary | ₦ Amount | What It Covers |

|---|---|---|---|

| Fixed Survival | 50% | ₦40,000 | Rent contribution, electricity, transport, food staples |

| Flexible Living | 25% | ₦20,000 | Airtime, data, personal care, eating out, entertainment |

| Emergency Buffer | 15% | ₦12,000 | Untouched unless a genuine emergency — not convenience |

| Savings / Goals | 10% | ₦8,000 | Locked immediately into PiggyVest, Cowrywise, or separate account |

The non-negotiable rule: Fixed Survival is paid the day salary arrives. Savings is locked the same day — not from “whatever is left,” because whatever is left never exists. Emergency Buffer stays untouched until you have built it to a meaningful amount.

If your salary is ₦50,000, the same percentages apply with smaller numbers: ₦7,500 saved every month becomes ₦90,000 in twelve months. That is your financial foundation.

Practical implementation tip: Open two accounts. Use your main account for spending. Use a separate PiggyVest or Cowrywise vault for your emergency buffer and savings. Money you cannot see at a glance is money you will not spend on impulse.

This one structural change is responsible for more salary management success in Nigeria than any other single habit.

Step 2 — Kill the 5 Silent Money Drains

These five categories quietly consume Nigerian salaries every single month. Identifying and plugging them is essential to any serious effort to stretch your salary to month-end.

1. POS and bank transfer charges. Nigerian workers pay an estimated ₦150–₦200 per POS withdrawal. At five withdrawals per week, that is ₦3,000–₦4,000 monthly in bank charges alone — money that buys nothing and goes nowhere. Fix: withdraw larger amounts once or twice a week instead of small amounts daily.

2. Untracked data and airtime. Most Nigerians cannot accurately recall what they spent on data last month. Track it for one month. The number will likely surprise you. Set a firm data budget of ₦3,500–₦5,000 per month and buy monthly bundles — daily or weekly bundles cost significantly more per gigabyte.

3. Impulse food spending. A plate of rice bought at a roadside seller costs ₦1,200–₦1,500 in most cities in 2026. Purchased every working day, that is ₦30,000–₦37,500 per month on lunch alone. This is not about never buying food outside — it is about assigning a fixed amount to it and being conscious when it is spent.

4. Unbudgeted family financial support. These requests carry emotional weight, which makes them among the hardest expenses to manage. But unplanned family support can drain ₦10,000–₦20,000 per month from a modest salary. The solution is to budget a fixed support amount — say ₦5,000–₦8,000 — and stop when it is reached. You cannot pour from an empty cup.

5. Forgotten subscriptions. DStv, Showmax, Netflix, a gym membership used once a month — list every recurring subscription and cancel anything you are not actively using at least once per week. Even ₦3,000–₦5,000 recovered here changes the end-of-month picture significantly.

Step 3 — Build Your ₦5,000–₦10,000 Emergency Buffer First

This single habit can break the borrow-every-month cycle for good.

Most Nigerians do not borrow to handle major disasters. They borrow to cover small, predictable surprises — a ₦4,000 NEPA bill that arrived early, a ₦3,500 emergency transport cost, a ₦6,000 pharmacy bill. These are the shocks that drive people to loan apps on the 18th of every month.

The solution is not a higher salary. It is a small float that absorbs small shocks before they become debt.

Target: ₦5,000 locked away and treated as non-existent. When you spend from it, replenish it before anything else in the following month. Grow it to ₦10,000, then ₦20,000 over time.

Real ₦ calculation: If you earn ₦60,000 per month and set aside ₦5,000 in month one and month two, you have your ₦10,000 buffer by month three. That ₦10,000 is the difference between a manageable problem and a loan.

This buffer is not a savings account. It is your personal shock absorber. Salary earner budgeting in Nigeria works most reliably when this buffer exists before any other financial goal is pursued.

Step 4 — Grocery and Food Strategy That Saves ₦10,000+ Monthly

Food is the category where intentional Nigerians consistently unlock the biggest savings — not by eating less, but by shopping differently.

Buy in bulk. A cup of parboiled rice from a roadside seller costs ₦1,800–₦2,000 in Lagos markets as of 2026. A 5kg bag costs ₦6,500–₦8,000 and feeds a single adult for two to three weeks. The per-meal savings are substantial when purchased ahead.

Cook in batches on weekends. Two hours on Sunday cooking a pot of stew, rice, and a side protein can eliminate five days of buying expensive cooked food. This is not sacrifice — it is a decision to keep your money working for your goals instead of someone else’s business.

Shop at open markets, not convenience stores. Tomatoes, peppers, onions, and crayfish at markets like Mile 12 (Lagos), Kugbo (Abuja), or any state-level market are typically 30–50% cheaper than the same items at a supermarket. Use convenience stores for urgent, specific items — not for bulk shopping.

Write a list before every shopping trip. Nigerians who shop without a list consistently overspend by ₦2,000–₦5,000 per trip on unplanned items. A shopping list costs nothing and works every single time.

Applying just these four food habits is enough to stretch your salary to month-end in Nigeria by recovering ₦10,000 or more that was previously spent without intention.

Step 5 — Transport and Data: Two Bills You Can Actually Control

Transport:

Bolt or Uber convenience has a serious hidden cost. A ₦2,500 ride taken every working day adds up to ₦65,000 per month on transport alone — more than many Nigerians earn in a month. The solution is not to stop using ride-hailing entirely, but to make it intentional. Use BRT, commercial buses, keke napep, or okada for predictable routine routes. Reserve app-based rides for late evenings, heavy loads, or safety-critical situations.

Set a fixed monthly transport budget and treat it as a hard limit. “Seeing how it goes” on transport spending always goes badly.

Data:

Nigerian mobile data pricing has seen slight stabilisation in 2026, but the behaviour around data remains expensive. Three specific habits to avoid:

- Buying data at convenience stores or vendor kiosks (consistently marked up 10–20%)

- Relying on daily or weekly bundles for heavy usage (most expensive per GB of any plan)

- Streaming on mobile data when Wi-Fi is available at work or a friend’s location

Buy your bundle at the start of the month, monitor usage via your network provider’s official app, and make any top-up from your Flexible Living budget — never from your Survival or Emergency allocations.

Controlling transport and data alone can add ₦8,000–₦15,000 back into your monthly budget — which goes a long way toward helping you stretch your salary to month-end in Nigeria every single month.

Step 6 — Say No to “Soft Life” Pressure Without Losing Your Sense of Self

This is the section that personal finance books written abroad never include.

In Nigeria, money is social. Your financial decisions are visible — and judged. Owambe invitations, birthday contributions, aso-ebi obligations, and “let us hang” pressure are all real economic forces that empty accounts faster than any single expense category. Managing them well is central to how to stretch salary to month-end in Nigeria without becoming isolated or resentful.

You do not need to disappear from social life. You need to budget for it.

Allocate ₦5,000–₦8,000 per month within your Flexible Living budget for social obligations. When that amount is spent, your social spending is done for the month. You have shown up, you have celebrated people, you have been present — that is genuinely enough.

For aso-ebi pressure specifically, this script works:

“I am working on some financial goals this period. I will absolutely show up to celebrate you — I just cannot buy the aso-ebi this time.”

Say it once, say it with warmth, and mean it. People who respect you will respect your boundary. People who do not respect it were leveraging your money, not your friendship.

The goal is not stinginess. It is trading the appearance of abundance for the reality of it — one month at a time.

What to Do When You’ve Done Everything Right and Still Fall Short

Here is the honest part that most budgeting guides skip.

Sometimes, even with a well-executed budget, life in Nigeria breaks the plan. Flood damage. A child hospitalised. A landlord who moved the rent date forward. A stolen phone that makes working impossible. These are not budgeting failures. These are life events. And in these moments, borrowing may be the correct decision — if it is done wisely.

When you must borrow, borrow strategically:

- Borrow only the exact amount you need — not the maximum you are approved for

- Compare interest rates and tenure across at least two lenders before accepting any offer

- Match the repayment date to your salary date — misaligned repayment dates are the fastest path to a debt spiral

- Avoid rolling over loans — repaying one loan with another compounds both the debt and the interest

- Verify the lender is FCCPC-listed — the Federal Competition and Consumer Protection Commission maintains a public register of approved digital lenders in Nigeria. Use it before downloading any new lending app.

For short-term, transparent salary bridging, LendSafe offers fast approval with clear repayment terms designed around the Nigerian salary cycle — no hidden deductions, no harassment, no surprises.

The goal, however, remains constant: borrow less with every passing month as your buffer grows and your system strengthens. Every naira you save toward your buffer is a naira that reduces how much you ever need to borrow.

Frequently Asked Questions

Q: What is a realistic savings amount on a ₦50,000 salary in Nigeria?

Starting with 10% — ₦5,000 per month — is realistic and achievable for most salary earners if the 4-part split is followed. That ₦5,000 per month becomes ₦60,000 in twelve months, which can fund a small business start, an emergency reserve, or a year-end personal goal.

Q: How do I handle months with extra expenses like school fees or NEPA arrears?

Create a “planned irregular expenses” category in your budget — sometimes called a sinking fund. Set aside ₦2,000–₦3,000 monthly toward predictable large annual bills. When the bill arrives, you are not surprised.

Q: Is it possible to save when my salary barely covers rent?

If your rent alone consumes more than 40% of your take-home salary, the structural problem needs addressing — whether that means negotiating a house with lower rent, taking a housemate, or exploring remote or hybrid work that reduces commute costs. Budgeting alone cannot fully solve a housing affordability problem, but the steps above will still stretch your salary to month-end in Nigeria further than doing nothing.

Q: What is the best savings app for Nigerian salary earners in 2026?

PiggyVest and Cowrywise are both well-established platforms that Nigerian salary earners use widely. PiggyVest’s SafeLock feature prevents premature withdrawal, which makes it particularly effective for emergency buffer building.

Final Word — The Goal Is to Borrow Less, Not Never

Nobody in Nigeria lives entirely free from financial pressure. The inflation rate — which the National Bureau of Statistics reported at elevated double-digit levels through 2025 — is real. Salaries have not kept pace with the cost of living. Family financial responsibilities do not shrink because income is modest.

The goal of every strategy in this guide is not perfection. It is direction.

Even if you save ₦3,000 this month instead of ₦8,000 — that is ₦3,000 more than you had. Even if you cook three days this week instead of zero — that is real money retained. Even if your buffer reaches only ₦5,000 by month three — that ₦5,000 may be the exact amount that keeps you from a loan next time an emergency strikes.

Learning how to stretch salary to month-end in Nigeria is not a one-day transformation. It is a monthly practice that compounds. Start with one section of this guide. Run it for thirty days. Add the next. Within three months, your salary will begin to behave differently — not because you earned more, but because you gave it a structure it never had before.

Your salary is not the problem. The system around it is. And systems can always be fixed.

Facing a short-term gap between a real need and your next payday? LendSafe offers fast, transparent personal loans for Nigerian salary earners — with no hidden fees, clear repayment schedules, and approval decisions that match your income cycle. Check if you qualify in two minutes.