The loan app said “not eligible.” The bank said “insufficient credit history.” You don’t know your exact score, but you know something is wrong — and you need to fix it before the next emergency hits.

This guide gives you a real plan to rebuild your credit score Nigeria-style. Not motivational fluff. Actual steps, in the right order, for the Nigerian credit system as it exists in 2026.

The Moment That Sends Most Nigerians Searching for This

You applied for a loan. You had your BVN, your phone number was active, your bank account was clean. But the app returned “sorry, we cannot process your request at this time” — or worse, the bank told you face-to-face that your credit profile was insufficient.

Maybe you defaulted on a loan two years ago and forgot about it. Maybe a previous loan app reported you without you realising. Maybe you’ve simply never borrowed before and have no credit footprint at all.

Whatever the reason, your ability to rebuild your credit score in Nigeria starts with understanding that this is not a permanent condition. It is a fixable data problem — and data problems respond to deliberate, consistent action.

Within 6 to 12 months of the right behaviour, you can move from “rejected” to “approved” — and eventually to better loan terms and lower interest rates. This guide shows you exactly how.

What a Credit Score Actually Means in Nigeria

Nigeria operates three licensed credit bureaus: CRC Credit Bureau, FirstCentral Credit Bureau, and CreditRegistry. Banks and most CBN-licensed loan apps query at least one of these before approving any loan application. Under the CBN Consumer Finance Policy, lenders are required to conduct credit checks before disbursing above a certain threshold.

Your credit score is a numerical summary of your borrowing history — whether you paid back loans on time, how much you currently owe, how many times lenders have queried your profile, and whether any lender has flagged you as a defaulter.

In Nigeria, scores typically range from 300 to 850 (structured similarly to the US FICO model):

| Score Range | Risk Level | Typical Lender Response |

|---|---|---|

| 700–850 | Low risk | Approved easily; access to better rates |

| 580–699 | Medium risk | Approved at higher rates or lower amounts |

| 300–579 | High risk | Rejected or very small amounts at maximum rates |

| No score | Unknown risk | Often rejected — no data to trust |

The painful truth: a significant portion of Nigerians who used early-generation loan apps — many of which the FCCPC investigated for predatory practices in 2022–2023 — may carry a negative bureau mark without knowing it. Learning how to rebuild credit score Nigeria often starts with discovering damage you didn’t know existed.

What Actually Damages Your Credit Score (Nigerian Real-Life Examples)

Before you rebuild, you need to know what broke it. These are the five most common causes:

1. Loan default or late repayment

You borrowed ₦15,000 from a loan app in 2022. Life happened. You didn’t pay back. The app reported you to CRC. That negative mark can remain on your file for up to 5 years if unresolved — affecting every loan application you make in the meantime.

2. Multiple hard inquiries in a short window

You applied to six different loan apps in one week hoping one would approve you. Each pulled your bureau report. Too many inquiries in a compressed period signals desperation to lenders and measurably pulls your score down. This is one of the most underappreciated ways borrowers damage their credit history in Nigeria.

3. High outstanding debt relative to income

If bureaus show ₦80,000 in active borrowing while your verified income is ₦60,000/month, your debt-to-income ratio looks dangerous. Lenders see this and decline — even if you’ve never technically defaulted.

4. Zero credit history

You’ve never borrowed a naira formally. Many lenders treat this the same as bad credit because there’s no data to base a decision on. Loan eligibility in Nigeria 2026 increasingly depends on having some credit footprint, not just a clean one.

5. Identity or data mismatches

Your BVN name doesn’t match your bank account name exactly. Small discrepancies can create fragmented profiles across bureaus or trigger flags that automated underwriting systems read as unreliable.

Step One: Check Your CRC Credit Report First (Don’t Skip This)

You cannot fix what you haven’t seen. Pulling your bureau report is the non-negotiable first move when you want to improve your credit score in Nigeria.

CRC Credit Bureau:

Visit https://crccreditbureau.com/ → click “Check Credit Report” → enter your BVN and personal details → pay the fee (typically ₦1,000–₦2,000) → download your full report. You can also walk into a CRC branch in Lagos (Victoria Island) or Abuja (Wuse II).

FirstCentral Credit Bureau:

Visit firstcentralcreditbureau.com and follow the same process. Several major Nigerian banks — including GTBank and Access Bank — offer free FirstCentral checks directly within their mobile apps. Check before paying.

What to look for in your CRC credit report:

– Any accounts marked “delinquent,” “default,” or “written off”

– Loan amounts that don’t match what you actually borrowed (potential identity fraud)

– Hard inquiry dates — how many lenders pulled your file and when

– Outstanding balances on loans you believed were fully settled

If you find an error: File a formal written dispute with the bureau. Under the Credit Reporting Act 2017, bureaus are required to investigate and respond within 21 business days. An incorrectly listed default that gets removed can move your score by a meaningful margin immediately — one of the fastest legitimate wins available when you want to rebuild credit score Nigeria-style.

Months 1–2: Stop the Bleeding

Before adding anything new to your credit record, you must stop making the existing damage worse.

Immediate actions:

- Stop applying to any new loan platforms for 30–60 days. Every application creates a hard inquiry. Nigerians in financial stress often apply to 10+ apps simultaneously — each one leaving a mark. This is counterproductive when you’re trying to rebuild your credit score in Nigeria.

- Settle outstanding loans, even partially. Contact lenders directly. Many will negotiate — particularly on debts older than 12 months. Even partial settlement changes the bureau status from “default” to “partially settled,” which reads meaningfully better to future lenders.

- Engage debt collectors, don’t avoid them. Ignoring recovery messages doesn’t make bureau entries disappear. Negotiating and settling — even at a discount — does.

- Correct BVN and identity mismatches. Visit a bank branch or your nearest NIMC registration centre. Name and date-of-birth corrections at the BVN level cascade through bureau records and can resolve fragmented profiles that were unknowingly suppressing your score.

Month 1–2 checkpoint: Zero new hard inquiries. At least one outstanding debt contacted for settlement discussion. CRC report downloaded and reviewed.

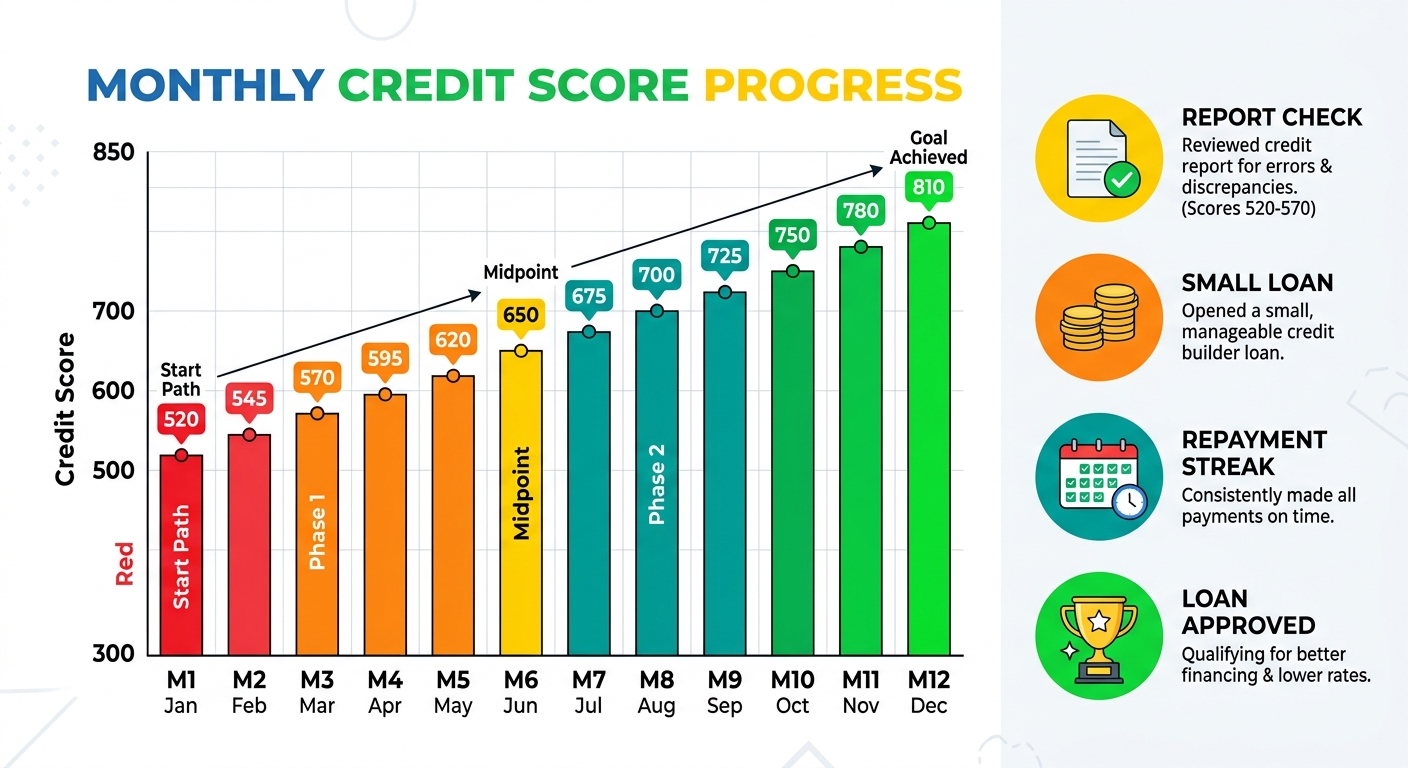

Months 3–4: Build Positive History Deliberately

Now you start adding clean, positive data to your credit file. This is where the real work of rebuilding your credit score Nigeria lenders will actually notice begins.

Borrow small, repay early — with the right lender.

Take a small loan — ₦5,000 to ₦15,000 — from a CBN-licensed lender that reports repayment behaviour to credit bureaus. This distinction matters enormously: many informal lenders and some loan apps only report negatives to bureaus (defaults), not positives. You need a lender that reports successful repayments too, so that your discipline actually shows up on your profile.

Repay before the due date, not just on it. Early repayment signals even stronger reliability than on-time repayment in some bureau scoring models.

Keep credit utilisation below 30%.

If a lender approves you for ₦30,000, borrow only ₦9,000–₦10,000. Using 80–100% of any approved credit limit damages your utilisation ratio — a key scoring variable — even when you repay on time.

Use your bank account consistently.

Regular salary inflows, predictable transaction patterns, and consistent account behaviour are being incorporated into alternative credit scoring models used by Nigerian fintechs. The NBS Financial Inclusion Survey 2023 noted that alternative data scoring now underpins a growing share of digital loan approvals — meaning your account behaviour matters beyond just bureau records.

Month 3–4 checkpoint: One successful small loan repaid early. Bank account active with consistent inflows. No new hard inquiries.

Months 5–6: Optimise for Loan Eligibility

By now you’ve reduced negatives and added at least one positive repayment entry. The next phase is about making your profile readable and trustworthy to lenders — the practical middle stage of any plan to rebuild credit score Nigeria borrowers can actually follow through on.

Maintain consistent contact details.

Keep the same phone number and primary bank account across all lender interactions. Lenders cross-reference data across systems — frequent number changes or account switches create discontinuity that automated underwriting reads as instability.

Space out any new loan applications.

If you need to apply to a new lender, wait a minimum of 45 days between applications. This prevents hard inquiry clusters — which visually signal desperation on any bureau report, regardless of your actual financial situation.

Build a three-repayment streak.

Three consecutive on-time repayments is the minimum threshold that begins to meaningfully shift your score in most bureau models. Treat reaching this milestone by end of Month 6 as your key performance indicator.

Month 5–6 checkpoint: Three on-time or early repayments recorded. Score check on CRC showing movement. No inquiry clusters.

Months 7–12: Sustain and Upgrade

This phase is about turning good behaviour into a permanent pattern that lenders can verify across multiple data points.

Increase loan amounts gradually and intentionally.

As your repayment track record develops, you become eligible for larger amounts. Request modest increases — move from ₦10,000 to ₦25,000, not from ₦10,000 to ₦150,000. Gradual escalation demonstrates controlled, purposeful borrowing behaviour. Sudden large requests after a period of small loans can trigger manual review.

Pull another bureau report at Month 9.

Check whether settled accounts have been updated correctly. Verify whether old default entries are approaching the 5-year removal window. Confirm your score bracket. If entries are still listed as “default” for debts you settled in Months 1–2, file a formal update request with supporting payment evidence.

Consider cooperative or salary-linked loan products.

Credit unions and registered cooperative societies often report to credit bureaus. A 6-month repayment record with a cooperative adds meaningful weight to your file and typically carries lower interest rates (12–24% annually for many cooperatives vs. 40–100%+ for some digital lenders). This is a significantly underused strategy when working to rebuild credit score Nigeria professionals and salary earners overlook.

Check your eligibility across multiple lender tiers.

By Month 12, if you’ve executed this plan consistently, your score should have moved at least one full bracket. That single bracket shift changes your loan eligibility in Nigeria materially: higher approved amounts, lower interest rates, and access to products that weren’t previously available to you.

What NOT To Do While Rebuilding (Mistakes That Reset the Clock)

These are the errors Nigerians most commonly make during credit rebuilding — each one sets you back months and undermines your ability to successfully rebuild credit score Nigeria lenders will respect:

- Don’t use a family member’s BVN or account to borrow on their behalf. This constitutes identity fraud, damages their credit history, and builds nothing in yours. Lenders are increasingly sophisticated at detecting proxy borrowing.

- Don’t pay “credit repair agents” who promise instant score improvement. No entity can legally remove accurate negative information before the statutory time limit expires under the Credit Reporting Act 2017. These agents take your money — typically ₦10,000–₦50,000 — and deliver nothing.

- Don’t close your oldest bank account. Even a low-activity account with a positive history contributes credit age to your profile. Closing it removes a trust signal that may have taken years to build.

- Don’t borrow to repay borrowing in a loop. Taking a ₦20,000 loan to repay a ₦15,000 loan while carrying ₦30,000 elsewhere increases both your total debt burden and your bureau utilisation simultaneously. This double-damage pattern is one of the primary traps that keeps Nigerian borrowers in the high-risk bracket for years beyond their original default.

- Don’t ignore your bureau report after settlement. Many Nigerians settle debts and assume the record updates automatically and correctly. It often doesn’t without follow-up. Always request and verify that the lender has reported the updated status to the relevant bureau.

The Bottom Line: Your Credit Score Responds to Consistent, Patient Behaviour

There is no 48-hour fix. There is no app that hacks your score back to 750 overnight. Anyone offering that is selling you something that will cost you money, damage your score further, or both.

What actually works when you want to rebuild your credit score in Nigeria is straightforward but requires patience: settle old debts through negotiation, borrow small from bureau-reporting lenders, repay early, space out applications, and pull your CRC credit report every quarter to verify that your positive behaviour is being recorded correctly.

Six months of consistent execution won’t make your profile perfect. But it will make it trustworthy — and trustworthiness is the only currency that lenders in Nigeria’s credit system actually respond to.

If you’re actively working on improving your credit score in Nigeria and need access to a transparent, CBN-licensed lender that reports positive behaviour to credit bureaus, the right starting point matters. Borrow what you need, repay on time, and let the record build itself — one repayment at a time.