Learning how to check your credit score in Nigeria is a critical step toward mastering your financial health. In today’s fast-paced digital economy, this single three-digit number can determine everything from your eligibility for an emergency loan to the interest rates you’re offered. Yet, many people are unaware this score exists or how to access it.

This ultimate guide demystifies the entire process. We’ll provide a step-by-step walkthrough to get your report from Nigeria’s official credit bureaus, understand what it means, and use it to your advantage.

What is a Credit Score and Why Does It Matter in Nigeria?

Think of your credit score as your financial report card. It’s a number, typically ranging from 300 to 850, that summarises your credit history and predicts your ability to repay borrowed money. The higher the score, the more financially trustworthy you appear to lenders.

This number is calculated based on information in your credit report, which details your borrowing and repayment activities.

Why it matters is simple: it determines your access to credit.

- Loan Eligibility: A good credit score is the key that unlocks loan approvals. Lenders, from large commercial banks to instant loan apps, use this score as a primary factor in deciding whether to lend you money.

- Better Interest Rates: A higher score doesn’t just get you approved; it gets you better deals. Lenders see you as a lower risk and are more likely to offer you lower interest rates, saving you thousands of Naira over the life of a loan.

- Faster Loan Processing: With a strong credit history, your loan applications can be approved much faster, which is critical when you need emergency funds.

- Increased Borrowing Power: As you build a positive credit history, lenders will be willing to trust you with larger loan amounts.

- Your Financial Identity: In the modern fintech landscape, your credit score is a core part of your financial identity. It proves your reliability and opens doors to a wider range of financial products and services.

Meet Nigeria’s Credit Bureaus: Who Holds Your Data?

Your financial data isn’t held by your bank alone. In Nigeria, the Central Bank of Nigeria (CBN) has licensed specific private companies called Credit Bureaus (or Credit Reporting Agencies) to collect, manage, and share credit information on individuals and businesses.

When you take a loan, miss a payment, or pay off a debt, financial institutions report this activity to the credit bureaus. These are the official gatekeepers of your credit information in Nigeria:

- CRC Credit Bureau Plc: One of the most prominent bureaus, CRC provides credit information services to a wide range of financial institutions. They are a popular choice for individuals looking to check their scores.

- FirstCentral Credit Bureau Limited: As the first licensed credit bureau in Nigeria, FirstCentral has a robust system for credit reporting and scoring, serving both lenders and consumers.

- XDS Credit Bureau Limited: XDS is another key player in the industry, contributing to the credit information ecosystem and promoting a more transparent lending environment.

These licensed credit bureaus are the legitimate sources for your official credit report and score.

Step-by-Step: How to Check Your Credit Score with CRC Credit Bureau

CRC Credit Bureau offers several convenient ways for you to access your credit information.

Method 1: Using the CRC Mobile App

- Download the App: Go to the Google Play Store or Apple App Store and download the “CRC Mobile” app.

- Register: Open the app and sign up as a new user. You will need to provide your personal details, including your full name, date of birth, and most importantly, your Bank Verification Number (BVN). Your BVN is crucial for accurate identity verification.

- Initiate Request: Once registered and logged in, navigate to the section for “Self Enquiry” or “Credit Report”. This process is known as a CRC self-enquiry.

- Make Payment: You will be prompted to pay a nominal fee (as of 2024, this is typically around ₦2,500, but is subject to change). You can pay securely within the app using your debit card.

- Receive Your Report: After successful payment, your credit report and score will be generated and delivered to your registered email address, usually within minutes.

Method 2: Using the CRC USSD Code

For a quick check without internet access, you can use the USSD service.

- Dial the Code: On your mobile phone, dial *565*8#.

- Follow the Prompts: The system will guide you through the process. You will need to enter your BVN and other personal details for verification.

- Confirm Payment: A fee will be deducted from your airtime balance. Ensure you have sufficient airtime before starting.

- Get Your Score: Your credit score will be sent to you via SMS. Note that this method usually provides just the score, not the full detailed report.

Step-by-Step: How to Check Your Credit Score with FirstCentral Credit Bureau

FirstCentral also provides a straightforward online portal for consumers.

- Visit the Website: Go to the FirstCentral consumer portal. This is their dedicated platform for individual credit checks.

- Create an Account: Register on their consumer portal. You’ll need to provide your personal data, including your BVN, for verification.

- Request Your Report: Once logged in, select the option to request your personal credit report. Look for the “check my score” or a similar button.

- Complete Verification: You may be asked a few security questions based on your credit history to confirm your identity.

- Access Your Report: After verification (and payment, if applicable), your credit report will be made available for you to view or download.

Can You Check Your Credit Score for Free in Nigeria?

Yes, you can.

According to a policy by the Central Bank of Nigeria (CBN), every Nigerian is entitled to one free credit report every year from each of the licensed credit bureaus.

This is a fantastic way to check in on your financial health annually without any cost. To claim your free report, you typically need to visit the bureau’s website (like FirstCentral or CRC) and look for the specific option for the “free annual credit report.” Any subsequent reports requested within the same year will require payment. This free report is a critical tool for routine financial monitoring.

Decoding Your Nigerian Credit Report: What to Look For

Getting your report is the first step; understanding it is the second. Here’s a breakdown of what you’ll find inside:

- Personal Information: Your name, address, date of birth, and BVN. Ensure all of this is accurate.

- Credit Summary: An overview of your total number of credit accounts (loan accounts, credit cards), total outstanding debt, and any negative indicators like public records.

- Credit History: A detailed list of all your credit accounts. This includes the lender’s name, the date the account was opened, the loan amount or credit limit, your current balance, and your repayment status for that account.

- Payment History: This is the most critical section. It shows whether you’ve paid your bills on time. Late payments, defaults, and collections are recorded here and significantly impact your score.

- Credit Inquiries: A list of who has accessed your credit report recently. “Hard inquiries” (from loan applications) can slightly lower your score temporarily.

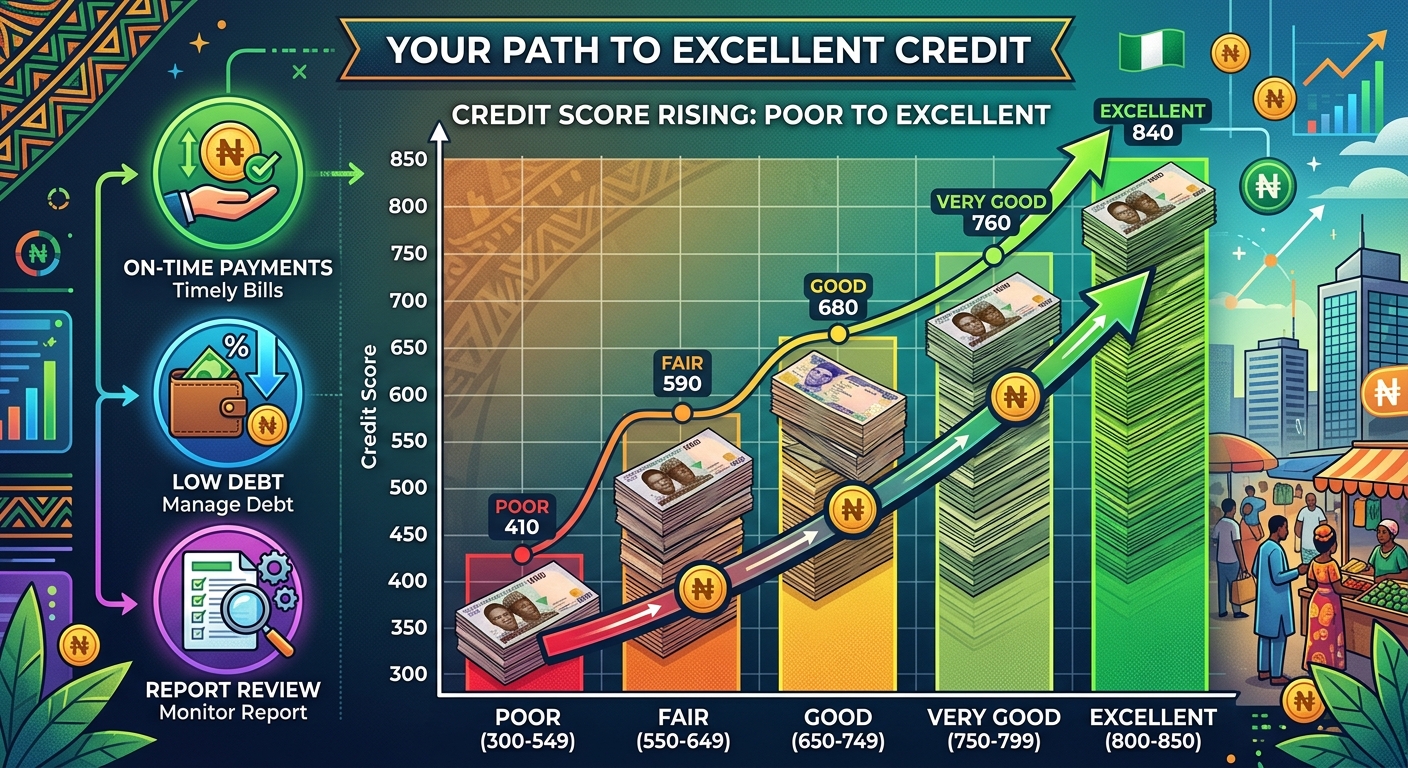

What is a Good Credit Score in Nigeria? (The Ranges Explained)

While the exact scoring models can vary slightly, the general score ranges in Nigeria are as follows:

- Excellent (760 – 850): You are a top-tier borrower. You will likely be approved for any loan you apply for at the best possible interest rates.

- Good (680 – 759): You are considered a very low-risk borrower. Lenders view you favourably, and you will have access to a wide range of credit products with good terms.

- Fair (620 – 679): You are seen as an acceptable risk. You can still get loans, but you may not be offered the best interest rates. This is a common range for many people.

- Poor (550 – 619): Lenders will view you as a high-risk borrower. You may struggle to get approved for loans from traditional banks, though some fintech lenders might still consider you at higher interest rates.

- Very Poor (300 – 549): It will be extremely difficult to obtain credit. This range indicates a history of major payment issues or loan defaults, signaling a very high risk to lenders.

5 Actionable Ways to Improve Your Credit Score

If you check your score and find it’s lower than you’d like, don’t panic. Your credit score is not permanent. Here’s how you can improve it:

- Pay Your Bills on Time, Every Time: This is the single most important factor. Set up reminders or automatic payments for all your debts, from digital loans to utility bills.

- Reduce Your Outstanding Debt: Try to pay down the balances on your existing loans. A lower debt-to-income ratio is very attractive to lenders and is a key part of effective debt management.

- Avoid Loan Defaults at All Costs: Defaulting on a loan is a major red flag that will severely damage your credit score for years. If you’re struggling to pay, contact your lender immediately to discuss options.

- Borrow Responsibly: Don’t apply for multiple loans at the same time. Each application creates a hard inquiry. Only take on debt that you are confident you can repay.

- Review Your Credit Report for Errors: Mistakes can happen. If you find an account that isn’t yours or an incorrect late payment entry, contact the credit bureau immediately to file a dispute and have it corrected.

Frequently Asked Questions (FAQs) About Nigerian Credit Scores

Q1: Can I check my credit score using just my BVN?

Yes, your BVN is the primary identifier used by credit bureaus to pull your financial data accurately from various institutions. All legitimate methods to check your score with a licensed bureau will require it.

Q2: Does checking my own credit score lower it?

No. When you check your own score (a “soft inquiry”), it has no impact. A “hard inquiry,” which happens when a lender checks your score as part of a loan application, can cause a small, temporary dip.

Q3: How often should I check my credit score?

It’s a good practice to check your credit report at least once a year (using your free annual report) to ensure everything is accurate and to monitor your financial health. If you are actively trying to improve your score or planning to apply for a major loan, you might check it more frequently.

Q4: Do all instant loan apps in Nigeria report to credit bureaus?

Most reputable fintech loan apps in Nigeria are now integrated with the credit bureau system. Taking a loan and repaying it on time can help build your credit history. Conversely, defaulting on a loan from these apps will negatively affect your score.

Conclusion: Your Credit Score is Your Financial Power

In today’s Nigeria, being ignorant of your credit score is a financial handicap. It’s no longer a hidden number used only by banks; it’s a vital tool that you can and should use to your advantage.

By understanding what your credit score is, checking it regularly, and taking proactive steps to improve it, you are not just managing debt—you are building a foundation for your financial future. Making the decision to check your credit score in Nigeria is the first step. You are taking control of your financial planning, opening doors to better opportunities, and empowering yourself on your journey to financial freedom. Take that step today.