When you search salary advance vs personal loan Nigeria, you are almost never doing research for fun. You need money. Something is due. And two product names keep appearing everywhere without anyone clearly explaining which one actually fits your situation right now.

This guide fixes that. By the time you finish reading, you will know which product matches your need, which one will cost you more than you expected, and how to decide in under 60 seconds.

The Friday Night Problem Every Nigerian Salary Earner Knows

It is Friday evening. Your landlord’s message came in this morning — rent is three days overdue. Your salary drops on the 25th, and today is the 18th. You have ₦4,200 in your account. Your children’s school fee deadline is Monday. NEPA cut the light off yesterday.

You open your phone. You see two options everywhere: salary advance and personal loan. They sound similar. They are not the same thing.

Picking the wrong one this weekend could cost you an extra ₦15,000 in fees — or worse, lock you into a repayment trap that eats into every salary for the next three months.

This guide breaks down the real difference between a salary advance and a personal loan in Nigeria, written specifically for salary earners, civil servants, corpers, and anyone whose income arrives once a month while life does not wait.

What Is a Salary Advance in Nigeria?

A salary advance — also called a payday loan — is a short-term loan extended against your next salary. The lender essentially says: “We know you will be paid on the 25th. We will give you part of that money now and collect it back the moment your salary drops.”

How It Typically Works:

- You borrow a percentage of your expected monthly salary — usually 50%–80%

- Repayment is deducted automatically from your salary account or via a standing order

- Loan duration is short: 7 to 30 days in most cases

- Approval is fast — sometimes under 10 minutes — because repayment risk is structurally low for the lender

Who Offers Salary Advances in Nigeria?

- Some employers through HR-backed advances at zero interest

- Commercial banks with active salary account relationships (GTBank, Access, and Zenith all have versions of this product)

- Fintech apps including FairMoney, Branch, QuickCheck, and LendSafe

- Workplace cooperative societies

The Critical Feature to Understand:

A salary advance is mechanically tied to your upcoming paycheck. If your salary is delayed — IPPIS backlog for civil servants, SUBEB payment gaps, or a private employer with cash flow problems — your repayment window becomes complicated fast. This is not a theoretical risk. According to the Nigeria Labour Congress, delayed salary payments affect millions of state government workers annually.

What Is a Personal Loan for Salary Earners?

A personal loan is a broader product. You borrow a fixed lump sum and repay it over an agreed schedule — 1 month, 3 months, 6 months, or longer. It is not tied to one specific payday.

How It Works:

- You apply and get assessed on BVN, credit history, and income verification

- You receive a lump sum disbursed to your bank account

- You repay in scheduled installments — weekly or monthly — over the agreed loan term

- Interest is calculated as either a flat rate or reducing balance, depending on the lender

Who It Works For:

- Someone who needs ₦100,000+ for a medical bill, not a ₦20,000 salary shortfall

- Someone whose emergency is larger than what one month’s salary can absorb

- Someone who wants to spread repayment so it does not consume an entire paycheck at once

- Artisans, contract workers, and people with irregular pay cycles who still demonstrate consistent income

The Important Distinction:

A personal loan gives you more money and more time. But more time means more total interest paid if you are not careful about the pricing structure — a point explored in detail below.

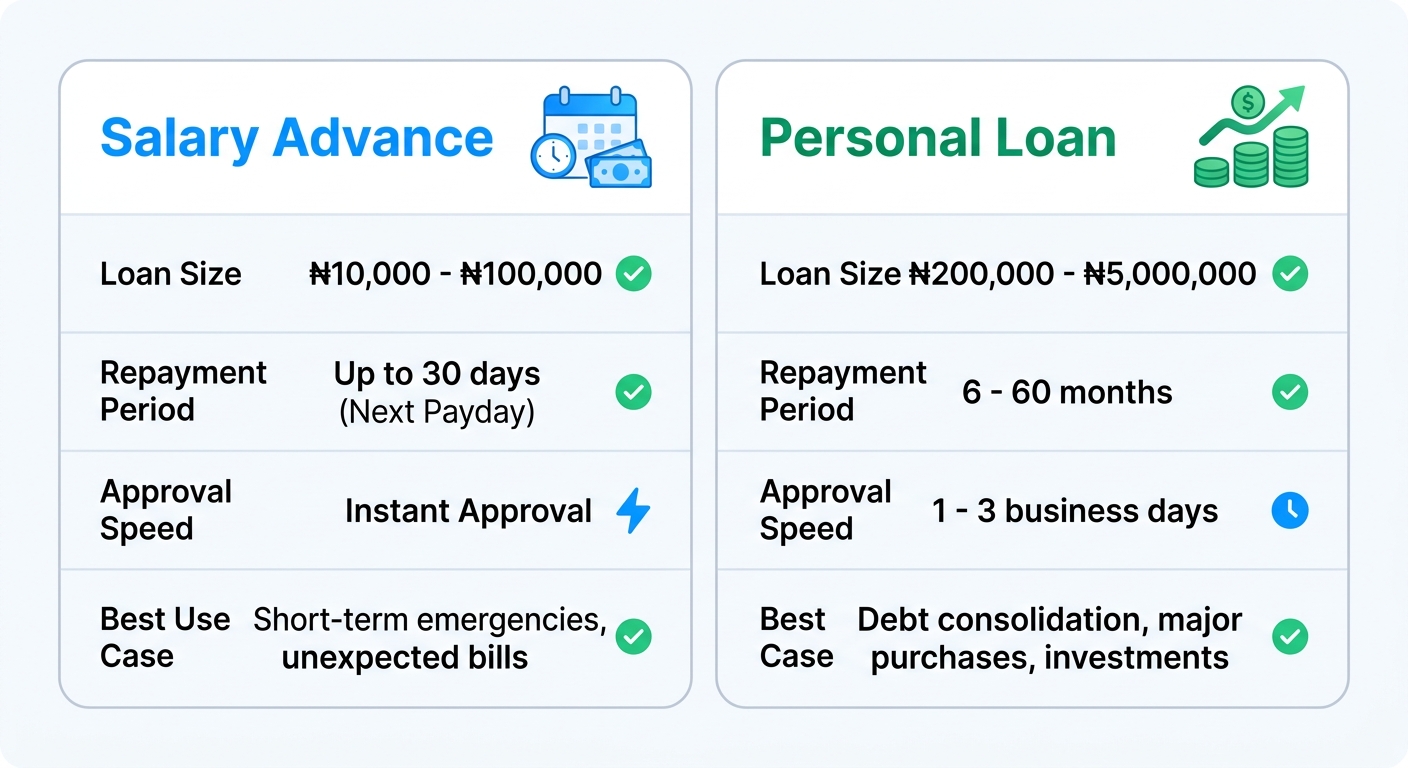

Side-by-Side Comparison: Salary Advance vs Personal Loan Nigeria

| Factor | Salary Advance | Personal Loan |

|---|---|---|

| Loan size | Usually 50%–80% of one salary | ₦10,000 – ₦5,000,000+ |

| Repayment period | 7–30 days | 1–24 months |

| Approval speed | Minutes to hours | Minutes to 24 hours |

| Interest structure | Flat fee or daily rate | Flat or reducing balance |

| Credit check intensity | Light (BVN + salary proof) | Moderate (BVN + credit history) |

| Who qualifies | Primarily formal salary earners | Broader — includes artisans, corpers, traders |

| Repayment method | Auto-deducted from salary account | Scheduled debit or bank transfer |

| Risk if salary delays | Missed repayment, penalty charges | Lower — schedule is pre-set |

| Best for | Small cash gap before next payday | Larger emergency, multi-month need |

| Worst for | Large or unpredictable emergencies | Tiny, short-term cash gaps |

When a Salary Advance Makes More Sense

Choose a salary advance if all three of the following conditions are true for your situation.

✅ Your need is small — a rent gap, utility bill, transport shortfall, or a school fee balance under ₦30,000 that a single salary deduction can cover comfortably.

✅ Your salary date is confirmed and close — within the next 7–20 days, and your employer has a reliable payment track record with no history of delays.

✅ You can absorb losing that portion of next month’s salary — meaning after the deduction, you will still have enough left to cover essential expenses until the following month.

Real Scenario Where a Salary Advance Wins:

Chukwuemeka works at a private school in Lagos. His salary is ₦85,000, dropping on the 28th. It is the 15th and his NEPA bill of ₦12,000 just arrived, threatening to disconnect his electricity. A salary advance of ₦15,000 costs him ₦1,800 in service fees — a total repayment of ₦16,800. On the 28th, the lender auto-collects from his salary account. Transaction complete. He still has ₦68,200 of his salary for the rest of the month.

That is a salary advance working exactly as designed.

When a Personal Loan Makes More Sense

Choose a personal loan if any of these apply to your situation.

✅ The amount you need is larger than your next salary — hospital bills, a broken generator that powers your business, unexpected travel, or school fees for multiple children.

✅ You need more than 30 days to repay comfortably — forcing a large loan into one repayment deduction will leave you depleted by day 5 of the following month, restarting the borrowing cycle.

✅ You are not a formal salaried employee — artisans, keke napep operators, market traders, and domestic workers may not have a predictable single payday, making salary advance structures structurally inaccessible.

✅ You want to protect your next salary from being swallowed whole — if you are a low-to-mid income earner, losing 60%–70% of your salary to one auto-deduction can trigger a cascading shortfall that forces another loan within two weeks.

Real Scenario Where a Personal Loan Wins:

Ngozi is a corper serving in Kogi State. Her monthly NYSC stipend is ₦33,000. Her mother had an emergency appendectomy — total hospital bill: ₦120,000. No salary advance product in Nigeria can solve this. She needs a personal loan of ₦120,000 spread over 5 months. At a flat monthly rate of 7%, her total repayment is approximately ₦162,000. Monthly installment: ₦32,400. That is manageable on her stipend. One giant single deduction of ₦120,000-plus from a ₦33,000 monthly income is mathematically impossible.

The Hidden Costs Most People Ignore

This section will save you real money if you read it carefully.

Salary Advance: The Rollover Trap

If your salary is delayed and you cannot repay on day 30, most Nigerian lenders charge a rollover fee or daily penalty interest. Several Nigerian loan apps charge between 1% and 2% per day on overdue balances. On a ₦20,000 advance, that is ₦200–₦400 every single day.

By day 14 of a salary delay — which happens regularly in state civil service — you have added between ₦2,800 and ₦5,600 to a loan you thought would be settled automatically. By day 30, you could owe more in penalties than you originally borrowed.

Always ask before borrowing: What is the daily penalty rate if my salary is delayed by even three days?

Personal Loan: The Flat Rate Illusion

Spreading repayment over 6 months sounds responsible and affordable. But if the lender charges a flat monthly rate, you pay that percentage on the original principal every month, not on the declining balance you actually owe.

Here is the math on a ₦100,000 personal loan at 10% flat monthly rate over 6 months:

- Monthly interest charge = ₦10,000 (10% of ₦100,000)

- Total interest over 6 months = ₦60,000

- Monthly repayment = ₦26,667 (principal ₦16,667 + interest ₦10,000)

- Total amount you repay = ₦160,000 on a ₦100,000 loan

That is not a scam. It is standard Nigerian consumer lending pricing. But a borrower who only reads the ₦26,667 monthly installment without calculating the ₦160,000 total has made an uninformed decision.

The Central Bank of Nigeria’s Consumer Protection Framework requires lenders to disclose the total cost of credit. Insist on this number before signing anything.

Always calculate: Total amount repayable — not just the monthly installment.

What Lenders Actually Check Before Approving Either Loan

Whether you are applying for a salary advance or a personal loan in Nigeria, legitimate digital lenders will verify the following:

BVN (Bank Verification Number) — Non-negotiable. Your BVN links your identity across all Nigerian bank accounts. The CBN mandated BVN enrollment precisely to reduce lending fraud. Any lender offering loans without a BVN check is either predatory or operating outside regulatory oversight.

Bank Statement or Salary Account Transactions — Lenders want to see consistent income credits. Three to six months of transaction history showing regular salary hits is often sufficient even without formal payslips. Open banking integrations now allow apps to read this data instantly with your permission.

Credit Bureau Data — Nigeria has three licensed credit bureaus: CRC Credit Bureau, FirstCentral Credit Bureau, and CreditRegistry. Lenders cross-check whether you have defaulted on previous loans. A negative record does not always mean outright rejection, but typically results in a smaller approved amount or a higher interest rate.

Employment Verification — For salary advances, some lenders require an employment confirmation letter or will call your HR department directly. Others rely entirely on bank statement analysis via open banking APIs, which is faster and more common among fintechs.

Smartphone Data Permissions (Fintech Apps) — Many Nigerian loan apps request access to contacts, SMS history, and app usage patterns. This is their alternative credit scoring model for users without formal credit histories. Understand exactly what you are consenting to before granting these permissions. The FCCPC has issued guidance on data access boundaries for digital lenders.

LendSafe Nigeria: What You Can Access

LendSafe is built for precisely these situations — the gap between what you need right now and your salary hitting your account.

On LendSafe, salary earners and individuals with verifiable income can access:

- Fast personal loans from ₦5,000 to ₦500,000

- Flexible repayment periods from 30 days to 6 months

- No physical collateral required

- Loan decisions in minutes based on BVN and bank statement analysis

- Transparent total-cost disclosure — you see the complete repayable amount before you confirm, not buried in a post-approval screen

LendSafe does not bury rollover penalties in fine print. The confirmation screen shows you what you pay — total. Whether your situation looks like a salary advance need (small, fast, short-term) or a personal loan need (larger amount, multi-month repayment), LendSafe structures the product to match your actual income and repayment capacity rather than offering one-size-fits-all terms.

You can also review additional borrowing options and compare loan structures through SmartLoans.ng to ensure you are selecting the right product for your specific financial position before committing.

Final Verdict: How to Decide in 60 Seconds

Answer these three questions honestly before you apply anywhere.

Q1: How much do I actually need?

– Less than 50% of my next salary → Lean toward salary advance

– More than my entire next salary → Personal loan, full stop

Q2: How soon can I realistically repay?

– Salary confirmed and arriving within 20 days → Salary advance may work

– Need 2–6 months to repay without financial strain → Personal loan

Q3: What does my budget look like after repayment?

– I can absorb the deduction and still cover rent, food, and transport → Either product can work

– Repayment will leave me immediately depleted → Longer-tenure personal loan, not a salary advance

The Rule That Will Save You Money Across Every Loan You Ever Take in Nigeria:

The most expensive loan is not the one with the highest interest rate. It is the one you take without understanding when and how much you are paying back.

Both salary advances and personal loans are legitimate, useful financial tools. The financial damage happens when someone takes a salary advance thinking it repays like a slow-burn personal loan — or takes a six-month personal loan for a ₦15,000 shortfall that resolved itself in two weeks, paying interest for months on a problem that no longer exists.

Know your numbers. Know your repayment window. Borrow smart.

Frequently Asked Questions

Can a civil servant in Nigeria get a salary advance through a fintech app?

Yes. Most digital lenders accept federal and state government employees. You will need your IPPIS number, a recent payslip, and a BVN-linked account that receives your salary. Processing is typically faster for federal employees because of more predictable payment cycles compared to some state governments.

Is a salary advance the same as a payday loan?

Functionally, yes. Both are tied to your upcoming paycheck and intended for short-term use. “Payday loan” is the internationally recognized term; “salary advance” is the more common phrasing in Nigerian banking and fintech contexts.

What is the maximum loan amount a salary earner can access in Nigeria?

This varies significantly by lender. Some fintech apps cap at ₦500,000 for first-time borrowers regardless of salary level. Banks with existing salary account relationships may approve multiples of monthly salary for long-standing customers. Your credit bureau record, employer type, and account history all influence the ceiling.

Does borrowing a salary advance affect my credit score in Nigeria?

Yes — both positively and negatively. Timely repayment builds a positive credit profile across the CRC, FirstCentral, or CreditRegistry bureaus. Defaults or late payments create a negative record that affects your ability to access loans in the future, including from banks.

LendSafe Nigeria is a digital lending platform operating in compliance with CBN consumer finance guidelines. All loan products are subject to eligibility assessment. Interest rates and terms are disclosed fully prior to confirmation. Borrow responsibly.