Knowing how to read loan terms in Nigeria is one of the most valuable financial skills you can develop — and one of the most overlooked. From bank branches to USSD codes to fintech apps, lenders are everywhere and they want your business. But speed and convenience have a dark side: millions of Nigerian salary earners sign loan agreements every year without fully understanding what they are committing to. The result is debt traps, salary garnishments, and credit score damage that could have been avoided with 30 minutes of careful reading.

This guide will show you exactly how to read loan terms in Nigeria — clause by clause, figure by figure — so you never pay more than you should.

Why Reading Loan Terms Matters: The Hidden Cost Problem

Here is a simple scenario that plays out every day in Nigeria.

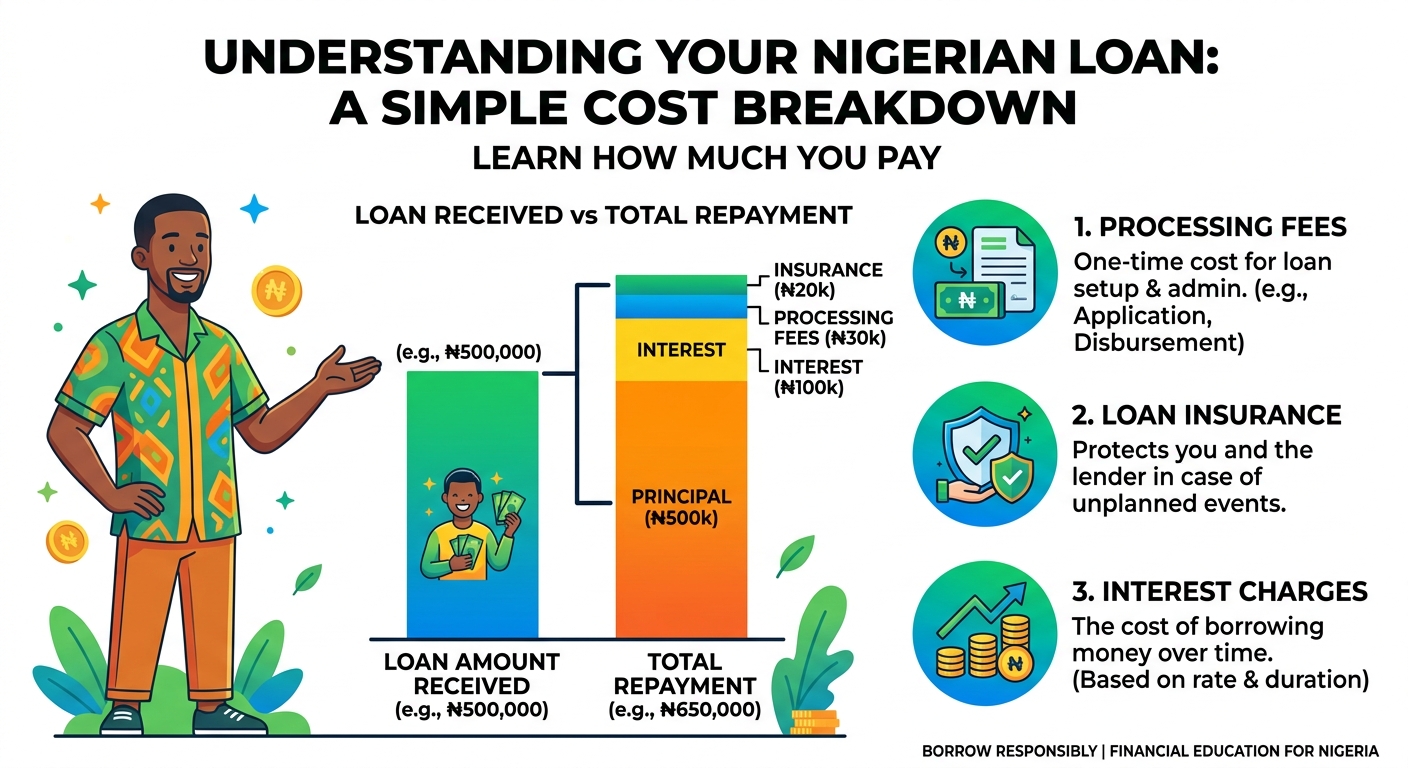

Emeka is a civil servant in Lagos earning ₦180,000 per month. He needs ₦300,000 for urgent home repairs. A digital lender advertises “3% monthly interest.” That sounds small, so Emeka signs without reading further.

What Emeka did not notice:

- Processing fee: 5% upfront = ₦15,000 deducted before disbursement

- Insurance fee: 2% = ₦6,000

- Monthly interest: 3% on the original ₦300,000 (not reducing balance) = ₦9,000/month

- Tenor: 6 months

Total repayment: ₦300,000 + (₦9,000 × 6) + ₦15,000 + ₦6,000 = ₦375,000

Emeka received only ₦279,000 in his hand but is repaying ₦375,000. His effective cost of borrowing is not 3% — it is closer to 34% for the 6-month period, or approximately 68% annualised.

This is not fiction. The Consumer Protection Department of the Central Bank of Nigeria (CBN) regularly receives complaints about undisclosed fees and misleading interest rate advertisements. The CBN’s Consumer Protection Framework (2016, revised 2022) specifically requires lenders to provide a Total Cost of Credit (TCC) disclosure before a borrower signs. If your lender is not showing you the TCC, that is your first red flag.

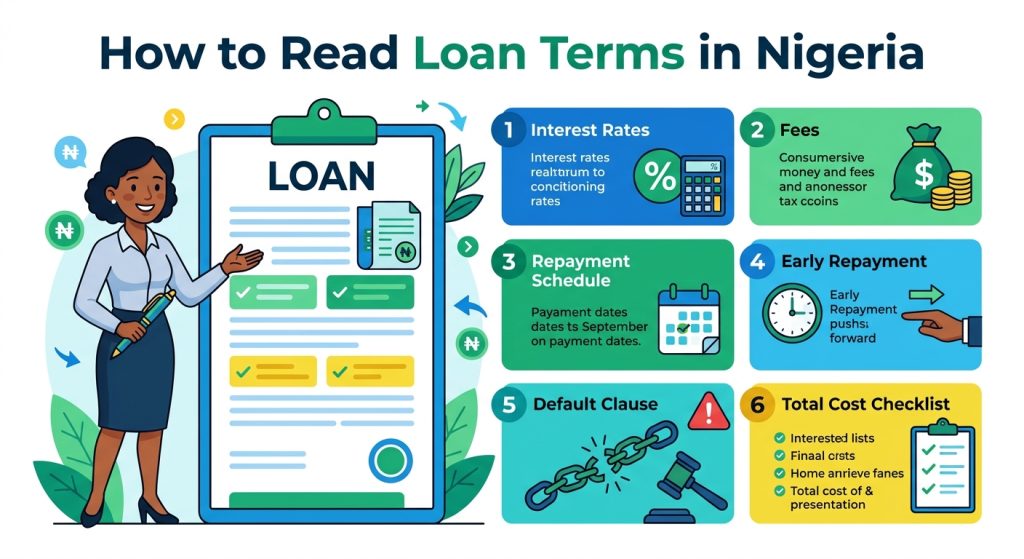

1. Interest Rate: Monthly vs Annual APR — How to Decode It

The single most manipulated number in any Nigerian loan offer is the interest rate. Lenders know that “3% per month” sounds friendlier than “36% per year,” even though they are mathematically equivalent on a flat-rate basis.

Flat Rate vs Reducing Balance

Flat rate means interest is calculated on the original loan amount every month, regardless of how much you have repaid.

Reducing balance (also called declining balance) means interest is calculated only on the outstanding principal.

Example:

Loan: ₦200,000 | Rate: 4% monthly | Tenor: 6 months

| Method | Total Interest Paid |

|---|---|

| Flat rate | ₦200,000 × 4% × 6 = ₦48,000 |

| Reducing balance | Approximately ₦27,000–₦29,000 |

The difference is nearly ₦20,000 on a single loan. Always ask: “Is this a flat rate or a reducing balance rate?”

Annual Percentage Rate (APR)

The APR is the most honest measure because it captures the true annualised cost including fees. Under the CBN’s guidelines and in line with the Federal Competition and Consumer Protection Commission (FCCPC) consumer rights framework, lenders are expected to clearly state the APR. If a lender only quotes a monthly rate, calculate the APR yourself:

Simple formula for flat rate:

APR ≈ Monthly rate × 12

For reducing balance:

Use the Internal Rate of Return (IRR) method or ask the lender directly. Never sign without knowing the APR.

If a lender refuses to state the APR in writing, walk away.

2. Fees: Processing, Insurance, Late Payment — What to Look For

Interest is only one line item. Nigerian loan agreements often contain several additional charges buried in fine print:

Processing/Origination Fee

This is charged upfront, often deducted from the loan before disbursement. It typically ranges from 1% to 5% of the loan amount. On a ₦500,000 loan, a 3% processing fee means you receive ₦485,000 but repay based on ₦500,000.

Key clause to find:

“A processing fee of X% shall be deducted from the principal at the point of disbursement.”

If it says “deducted,” your net disbursement is lower — adjust your repayment calculations accordingly.

Insurance/Credit Life Fee

Many lenders bundle in insurance (credit life or loan protection). While this can be legitimate, it should be optional or clearly disclosed. Insurance fees of 1%–3% on top of the principal are common. Ask for the insurance certificate and verify the underwriter is registered with the National Insurance Commission (NAICOM).

Late Payment Penalties

This is where borrowers get hit hardest. Common structures include:

- Flat daily penalty: ₦500–₦2,000 per day of delay

- Percentage penalty: 1%–5% of the overdue amount per month

- Compounding penalties: Late fees added to principal, then interest charged on the new total

Example clause to watch for:

“Overdue payments shall attract a penalty of 2% per month on the outstanding balance, compounded monthly.”

On a ₦100,000 overdue balance, this is ₦2,000 in month one — but if it compounds, month two is ₦2,040, month three ₦2,081, and the debt grows without end.

3. Repayment Schedule: Bullet vs Instalment, What “Tenor” Means

Tenor

“Tenor” simply means the duration of the loan — the period over which you are expected to repay. A 6-month loan has a tenor of 6 months. Always confirm whether your tenor is in days, weeks, or months, because some digital lenders use “30-day” or “90-day” tenors that can catch salaried workers off guard.

Instalment (Amortising) Loans

You repay in equal periodic payments (usually monthly) that cover both principal and interest. This is the most common structure for salary earners and the most manageable. You should receive an amortisation schedule — a table showing every payment, how much goes to interest, and how much reduces the principal.

If your lender cannot produce this table, ask for it. It is your right.

Bullet Repayment

The entire principal plus interest is due on one date at the end of the tenor. This is common for short-term bridge loans. If you take ₦200,000 with a 6-month bullet structure at 5% monthly (flat), you owe ₦260,000 in one lump sum at month six. Miss that date and penalties begin immediately.

Bullet loans are high-risk for salary earners. Only take one if you are certain of a lump sum income by that date — a contract payment, bonus, or gratuity.

For a deeper look at choosing the right loan structure for your income level, read our guide on responsible borrowing strategies for Nigerian salary earners.

4. Early Repayment Clause: Is There a Penalty?

This is one of the most overlooked sections in any Nigerian loan agreement, and it can cost you money even when you are doing the right thing.

Some lenders — particularly those using flat-rate structures — charge an early repayment penalty because paying early cuts into their expected interest income.

Common clause language:

“Early termination of this facility shall attract a prepayment penalty of 2% of the outstanding principal, in addition to accrued interest to date.”

What This Means in ₦ Terms

You borrow ₦400,000 for 12 months at 3% monthly (flat). After 6 months, you have a windfall and want to pay off the ₦200,000 remaining principal. If the contract has a 2% prepayment penalty:

- Remaining principal: ₦200,000

- Penalty: ₦4,000

- Accrued interest to date (already factored into instalments, but some lenders claim additional “earned interest”)

Always ask: “If I pay off this loan early, exactly what do I owe?” Get the answer in writing before you sign.

If there is no early repayment clause, or it says “no penalty for early repayment,” that is a borrower-friendly contract. Note it as a positive.

5. Default Clause: What Happens Legally If You Miss Payments

The default clause is the most legally consequential section of any loan agreement. In Nigeria, defaulting on a loan can trigger several consequences:

Salary Domiciliation

Many banks and employer-linked lenders include a salary domiciliation clause — meaning your employer is directed to remit your salary directly to the lender until the debt is cleared. This is legal when you have signed a consent form.

Clause to identify:

“The Borrower hereby irrevocably authorises the Employer to deduct monthly loan repayments from the Borrower’s salary and remit same to the Lender.”

If you sign this, your employer becomes the lender’s collection agent. Understand the implications before agreeing.

Credit Bureau Reporting

Nigeria operates three licensed credit bureaus: CRC, FirstCentral, and CreditRegistry. Under the CBN Credit Reporting Act (2017), lenders are required to report defaults. A default on your credit report can affect your ability to access any formal credit for 3–7 years.

The FCCPC also has provisions under the Federal Competition and Consumer Protection Act (FCCPA) 2018 that regulate how lenders communicate defaults and handle debt recovery. Aggressive or harassing recovery tactics — such as contacting your employer without authorisation, or public shaming via social media — are violations you can report to the FCCPC.

Legal Action and Asset Recovery

For secured loans, default can trigger seizure of collateral (property, vehicles). For unsecured loans, the lender may proceed to a Magistrate or High Court for a money judgment, after which they can attach your bank accounts.

Know this before you sign: The default clause should clearly state the cure period — typically 7 to 30 days — before the lender can take enforcement action. If the clause says “immediate default upon any missed payment” with no cure period, negotiate or choose another lender.

To explore lenders with transparent, borrower-friendly default terms, visit SmartLoans.ng for a comparison of regulated loan options in Nigeria.

6. Quick Checklist Before You Sign

Use this checklist every time. It takes less than 15 minutes and can save you tens of thousands of naira.

✅ Pre-Signing Loan Review Checklist

| # | What to Check | What to Look For |

|---|---|---|

| 1 | Total Cost of Credit (TCC) | Is it stated in ₦, not just percentages? |

| 2 | Interest Rate Type | Flat or reducing balance? Monthly or annual? |

| 3 | APR | Is it explicitly stated? Calculate it if not. |

| 4 | All Fees | Processing, insurance, stamp duty, legal fees — list all |

| 5 | Repayment Schedule | Is an amortisation table provided? |

| 6 | Tenor | Days, weeks, or months? Bullet or instalment? |

| 7 | Early Repayment | Is there a prepayment penalty? How much? |

| 8 | Late Payment Penalty | Flat or compounding? Daily or monthly? |

| 9 | Default Clause | What is the cure period? What triggers default? |

| 10 | Salary Domiciliation | Have you consented? Do you understand implications? |

| 11 | Credit Bureau Clause | When and how will defaults be reported? |

| 12 | Lender Registration | Is the lender licensed by CBN or registered with FCCPC? |

Final Word: Your Signature is Your Commitment

In Nigerian consumer finance, the burden of understanding a contract falls on the borrower the moment you sign. Courts will generally enforce what you agreed to — even if you did not read it. The CBN and FCCPC provide frameworks for recourse, but prevention is always better than a complaint process.

The good news is that reading loan terms is a skill, not a talent. The six areas covered in this guide — interest rates, fees, repayment structure, early repayment, default consequences, and total cost — cover approximately 90% of what matters in any Nigerian loan agreement.

Do not let urgency push you into carelessness. A lender who pressures you to sign immediately without reading is a lender you should not be borrowing from.

Know what you are signing. Know what it costs. Borrow responsibly.

For personalised guidance on choosing regulated lenders with transparent terms, visit SmartLoans.ng. For complaints about predatory lending practices, contact the FCCPC or the CBN Consumer Protection Department.