The Moment Most Nigerians First Think About a Personal Loan

It usually hits on a Tuesday.

Your landlord’s message lands at 7:43 AM: “Oga, this month you must pay or I will change the padlock.” Your salary won’t hit until the 25th. It is the 9th. You have ₦4,200 in your account, a data bundle running low, and a school fee reminder sitting in your email.

Or your okada broke down. Your child’s hospital bill arrived and NHIS covered almost nothing. Your mother called from the village.

In every one of those moments, the same question forms: “Where can I get money fast — and is it safe?”

That question is exactly what this guide answers — completely, without jargon, and without fine print buried in footnotes. Whether you have never taken a personal loan Nigeria lenders offer before, or a previous one went badly, this is the guide you should have read first.

What Is a Personal Loan in Nigeria? (Plain English Definition)

A personal loan Nigeria borrowers take is money a lender gives you today, which you agree to repay over a fixed period — usually with interest added on top.

It is not a business loan. Not a mortgage. Not an investment vehicle. It is cash for your personal life — rent, hospital bills, school fees, food, transport, broken appliances, or a family emergency. You receive the money, use it for whatever personal need you have, and repay it in scheduled instalments.

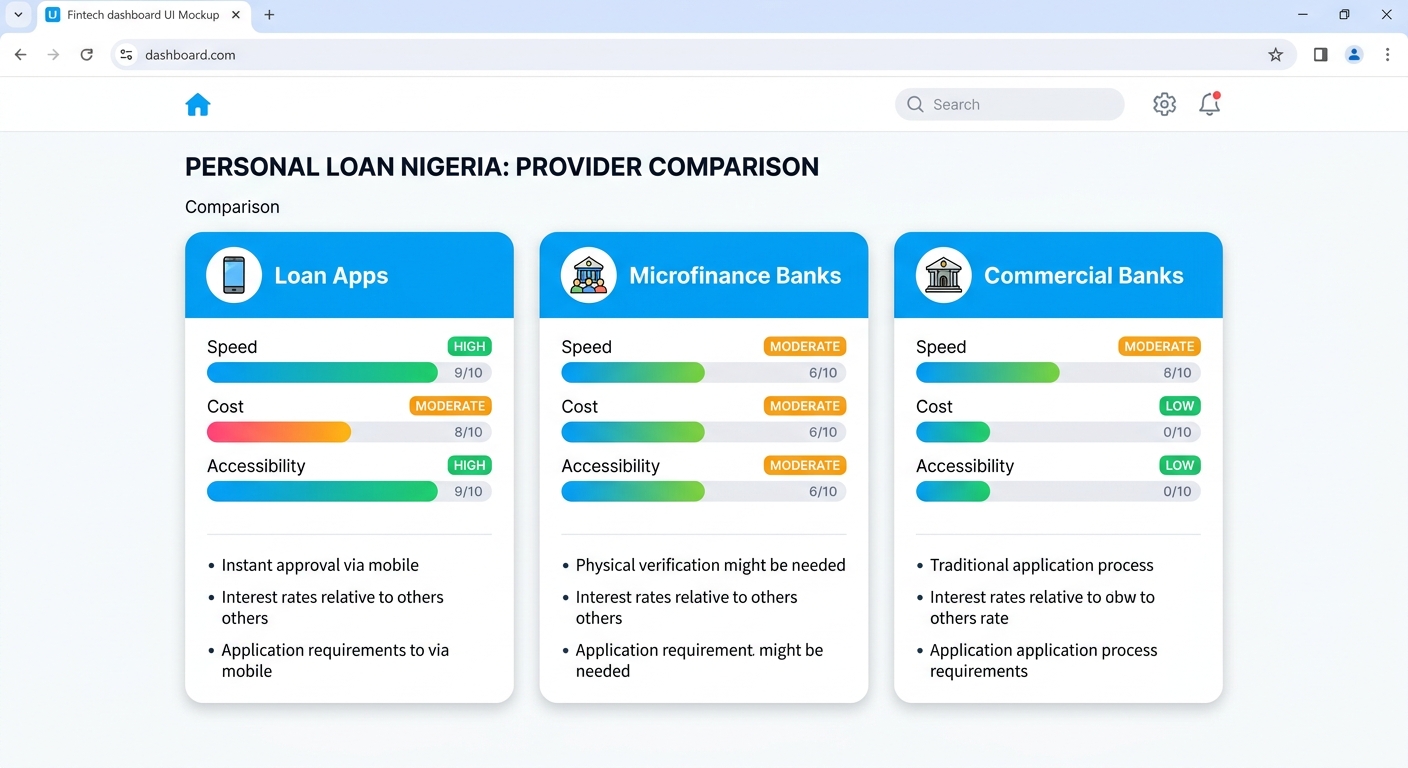

In Nigeria, personal loans come from three main sources:

- Commercial banks (Access, GTBank, UBA, First Bank — typically slower, more paperwork-heavy)

- Microfinance banks (more flexible for low-income earners, regulated by the Central Bank of Nigeria)

- Licensed digital loan apps (fastest, most accessible — where most Nigerians now borrow)

The digital loan app category has grown aggressively since 2020. According to the FCCPC’s Digital Lending Report, over 160 digital lenders were reviewed, reflecting the massive scale of app-based personal loan activity in Nigeria. Platforms like Carbon, FairMoney, Branch, and SmartLoans disburse funds in minutes — directly to your bank account — using your BVN, phone number, and basic income verification.

Who Actually Qualifies for a Personal Loan in Nigeria?

This surprises most first-time borrowers: the qualification bar is lower than you think. You do not need to own property. In many cases, you do not even need a payslip.

| Borrower Type | What Lenders Check |

|---|---|

| Salary earner (private sector) | Regular account inflow, BVN, employer verification |

| Government employee / civil servant | Salary account, IPPIS number (for some lenders) |

| NYSC corps member | Allawee deposits, BVN, phone number |

| Artisan / self-employed | Account cash flow history (3–6 months), BVN |

| Market trader | Account activity, BVN, sometimes a guarantor |

| Student | Very limited — some apps allow small amounts with BVN only |

The practical reality is that digital lenders evaluate your account behaviour — how money flows in and out — rather than paper documents alone. This is what makes a personal loan Nigeria residents with informal income can access genuinely different from traditional bank lending, which excludes millions of Nigerians who earn well but lack formal documentation.

Types of Personal Loans Available in Nigeria

Not every personal loan Nigeria lenders offer is built the same. Knowing the differences saves you real money and prevents you from borrowing the wrong product for your situation.

a) Salary Advance Loans

Short-term bridge loans designed to cover the gap between now and your next payday. Usually 14–30 days. Higher daily interest rate, but manageable total cost if used correctly. Best for small, urgent, short-cycle shortfalls.

b) Instalment Personal Loans

You borrow a larger amount and repay in equal monthly instalments over 3, 6, or 12 months. Total absolute cost is higher, but monthly payments are more manageable. Best for school fees, rent, medical bills, or appliance replacement.

c) App-Based Nano Loans

Small amounts — ₦5,000 to ₦50,000 — disbursed in minutes. Repayment is typically 7 to 30 days. Best for end-of-month shortfalls, data, transport, or food emergencies.

d) Bank Personal Loans

Larger amounts, longer tenors (up to 48 months), lower monthly rates — but require formal documentation, salary domiciliation, and a processing period of days or weeks. Best for salary earners with time to spare and non-urgent needs.

e) BNPL (Buy Now Pay Later)

Not a cash loan — it lets you purchase a product and spread repayment. Useful for appliances and devices but does not put cash in your hand.

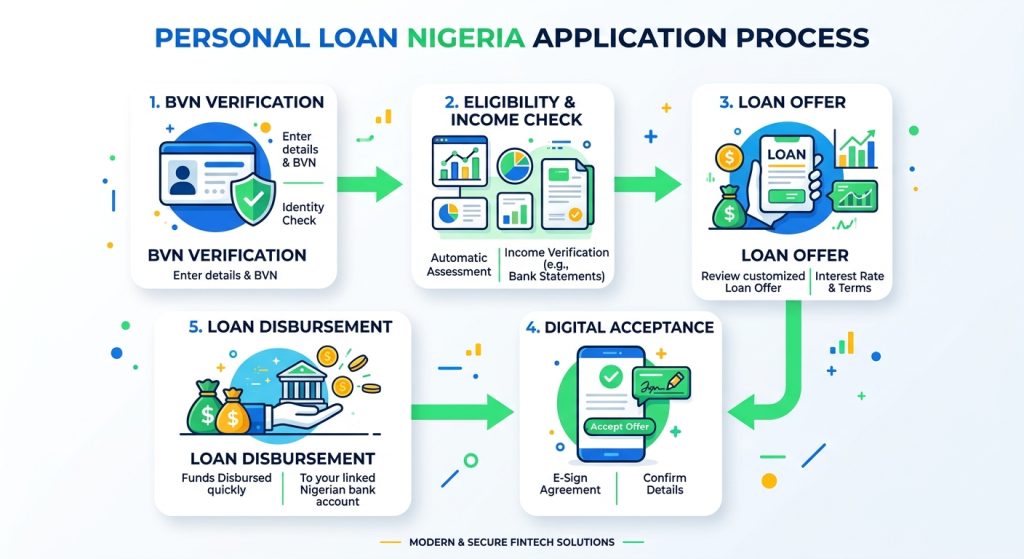

How the Application Process Works — Step by Step

If you are applying through a licensed loan app — the fastest and most common route for a personal loan Nigeria residents choose — here is exactly what happens:

Step 1: Choose a registered lender.

Before downloading anything, verify the lender on the FCCPC’s registered digital lenders list. Fake apps exist and cause real harm. This step takes 60 seconds and can save you everything.

Step 2: Create your account.

Your phone number and BVN are the foundation. Basic personal details — name, address, occupation — are collected at this stage.

Step 3: BVN verification.

The app links your BVN to verify your identity and performs a soft credit check through CRC Credit Bureau or FirstCentral Credit Bureau. This does not damage your credit score.

Step 4: Account and income analysis.

Many apps request your bank statement or direct account linkage. They analyse inflow patterns to determine a safe borrowing limit for your personal loan.

Step 5: Review your loan offer.

The platform presents an offer: amount, interest rate, repayment date, and — critically — the total repayable amount. Read every number. Do not tap “Accept” until you understand the full cost, not just the monthly instalment.

Step 6: Disbursement.

Accept the offer and money hits your account. For most licensed apps offering a personal loan Nigeria borrowers trust, this takes 5 to 30 minutes on the first application.

Total time from download to cash in your account: as little as 20 minutes.

What Lenders Actually Check — The 5 Real Criteria

When you apply for a personal loan Nigeria lenders assess, they are silently evaluating five things simultaneously:

- Identity verification — Is your BVN authentic? Does it match your account? Are you flagged for fraud on any bureau?

- Income pattern — How consistently does money enter your account? What is the average monthly inflow over the past three months?

- Credit history — Have you defaulted on a previous loan? Do you have multiple active loans running right now?

- Debt-to-income ratio — What percentage of your monthly income is already committed to existing loan repayments?

- Device and behavioural signals — Many apps analyse phone usage patterns and app behaviour (with your permission, granted when you accept the terms) to lend to people with thin formal credit files.

The thing lenders don’t advertise: If you have three active loans running simultaneously when you apply for a new personal loan, your approval odds drop sharply — even if you are repaying all three on time. Multiple active debts signal cash flow stress, and lenders respond by either declining the application or reducing the offered amount significantly.

How Much Can You Borrow — and What Does It Actually Cost?

Typical borrowing ranges in Nigeria (2026):

- First-time app borrowers: ₦5,000 – ₦100,000

- Returning borrowers with a clean personal loan repayment history: ₦100,000 – ₦500,000

- Commercial bank personal loans (formal employment required): ₦200,000 – ₦5,000,000+

Typical personal loan interest rates Nigeria (2026):

| Lender Type | Monthly Rate |

|---|---|

| Licensed loan apps | 3% – 10% per month |

| Microfinance banks | 4% – 8% per month |

| Commercial banks | 2% – 4% per month |

Real naira calculation — always use total repayable, not monthly rate:

Scenario A: Borrow ₦50,000 for 30 days at 10% monthly interest.

Interest = ₦5,000 | Total repayable = ₦55,000Scenario B: Borrow ₦100,000 for 3 months at 5% flat monthly interest.

Total interest = ₦15,000 | Total repayable = ₦115,000

The monthly rate sounds small in isolation. The total repayable is the number that actually matters for any personal loan Nigeria platforms offer — always request it explicitly before accepting any loan offer.

For a complete breakdown of how personal loan interest rates are structured in Nigeria, see our dedicated guide on loan interest rates and repayment calculations at SmartLoans.ng.

Personal Loan vs Your Other Borrowing Options — Quick Comparison

| Option | Speed | Cost | Risk | Best For |

|---|---|---|---|---|

| Licensed personal loan app | 🟢 Minutes | 🔴 High per month | 🟡 Medium | Urgent, short-term needs |

| Salary advance from employer | 🟢 Fast | 🟢 Low/free | 🟢 Low | Salary earners only |

| Bank personal loan | 🔴 Days–weeks | 🟢 Lower monthly | 🟢 Low | Larger, non-urgent needs |

| Co-operative society | 🟡 Days | 🟢 Low | 🟢 Low | Members only |

| Family / friend | 🟢 Instant | 🟢 Zero interest | 🟠 Social risk | Trusted relationships |

| Unlicensed lender (agbero/shylock) | 🟢 Instant | 🔴🔴 Extreme | 🔴🔴 Very high | Avoid always |

The licensed personal loan Nigeria app wins on speed. Everything else wins on cost. Your specific situation — urgency, income type, documentation availability — determines which trade-off is right for you.

Red Flags to Avoid Before You Sign Anything

Nigeria’s personal loan market contains many legitimate operators and a dangerous minority of predatory ones. Here is how to separate them before you share your BVN or bank details:

🚩 The lender is not listed on the FCCPC registered digital lender database — this is the single most important check before applying for any personal loan Nigeria lenders advertise

🚩 They request an upfront “activation fee” or “processing fee” — legitimate lenders deduct any applicable fees from the disbursed amount; they never demand money before you receive your loan

🚩 No physical address, no verifiable customer service line, no FCCPC registration number displayed within the app

🚩 They threaten to contact your phonebook before you have even defaulted — this practice was explicitly prohibited by the FCCPC in its 2022 digital lending regulations

🚩 The total interest and fees are not shown to you before you accept the offer

🚩 The app requests unrestricted access to all your contacts, photo gallery, and messages — FCCPC-compliant personal loan Nigeria platforms are required to limit data collection to what is strictly necessary for lending

How to Repay Without Falling Into a Debt Spiral

The biggest mistake Nigerian borrowers make is not defaulting — it is reborrowing to cover the repayment of the previous personal loan.

The spiral looks like this:

Borrow ₦30,000. Repayment due = ₦34,500. Salary delayed by five days. Take a second ₦34,500 personal loan to settle the first. Now owe ₦39,675. Salary arrives but is fully absorbed by the new repayment. Take a third loan for food and transport. The cycle locks in.

This is not stupidity. It is what happens when a personal loan treats a symptom — a cash gap — without addressing the underlying cash flow pattern that created the gap in the first place.

Five ways to repay a personal loan Nigeria borrowers often overlook:

- Budget the repayment before you borrow — if your next salary cannot cover the full repayment and still leave you functional for the month, reduce the loan amount until it can

- Set your repayment date to match your exact pay date — most licensed apps allow you to select this date during the application process

- Repay early when possible — many lenders charge personal loan interest only for the days the loan is active, so early repayment directly reduces your total cost

- Do not take a new personal loan the same week you repay an old one unless a genuine new emergency has occurred

- Build a micro-buffer — after repaying, save ₦1,000 per week into a separate savings app; over 12 weeks, this builds a ₦12,000 emergency reserve that eliminates the need to borrow for food, transport, or data entirely

How SmartLoans.ng Fits Into This Landscape

SmartLoans.ng is a licensed personal loan Nigeria platform built specifically for Nigerians who need fast, transparent borrowing — not a debt trap packaged as a lifeline.

Here is what sets it apart:

✅ Full cost disclosure before acceptance — you see the total repayable amount, not just the monthly rate, before you commit to any personal loan

✅ No contact harvesting — SmartLoans.ng does not access or weaponise your phonebook contacts

✅ Repayment dates that align with your pay cycle — you choose a date that works for your income, not a date that works for the lender

✅ Credit bureau reporting on every repayment — every on-time personal loan payment improves your credit profile with CRC Credit Bureau, which expands your future borrowing power

✅ FCCPC registered, CBN-compliant operations

SmartLoans.ng is not marketed as the cheapest personal loan Nigeria has to offer — no responsible lender providing speed and accessibility without collateral will ever be the cheapest option. But in a market crowded with hidden fees and harassment tactics, transparency is a more valuable feature than a marginally lower rate.

Final Verdict: Should You Take a Personal Loan in Nigeria?

Yes — if:

– The need is real and urgent (rent, medical bills, school fees, essential equipment replacement)

– You have a clear income source that comfortably covers the full repayment

– You are borrowing from a licensed, FCCPC-registered lender

– You have read and fully understood the total repayable amount before accepting

No — if:

– You are taking a personal loan to repay another loan

– You have no confirmed repayment source in the immediate income cycle

– The lender has not disclosed the full cost upfront

– You feel pressured, rushed, or confused by the terms being presented

A personal loan Nigeria borrowers use wisely is a financial tool — nothing more, nothing less. Used in the right situation, with the right licensed lender, at the right loan amount, it solves a real problem today without creating a larger one next month. Used carelessly, it creates precisely the crisis it was supposed to prevent.

You now know enough to use it correctly.

→ Check what you qualify for in 3 minutes. Visit SmartLoans.ng to get a transparent personal loan offer — with full cost disclosure before you commit to anything.

SmartLoans.ng operates in compliance with CBN guidelines and FCCPC consumer protection regulations. All personal loan offers are subject to eligibility assessment. Borrow responsibly.