You Needed ₦20,000. Now They’re Calling Your Pastor.

You downloaded the app because your data ran out and your landlord was calling. The loan came in 4 minutes. You exhaled.

Then you missed one repayment — just one — and everything changed.

Your mum got a call. Your colleague at the office got a message with your photo attached, saying you were a fraudster. Your WhatsApp contact list became a weapon pointed at your reputation.

This is not a horror story. This is what predatory lending in Nigeria looks like in 2026 — and it is happening to real people every single week.

This guide will show you exactly how to spot a predatory lender before you borrow, what to do if you are already inside a debt trap, and which authorities in Nigeria actually have the power to help you.

What Is Predatory Lending?

Predatory lending in Nigeria is when a lender deliberately structures a loan under conditions designed to trap you — not help you.

The trap works like this: the terms are confusing or deliberately hidden, the interest compounds faster than you expect, and the consequences of missing a payment go far beyond money. These loan sharks in Nigeria attack your dignity, your relationships, and your employment.

Predatory lenders are not just street-corner operators. Many run polished apps available on the Google Play Store with professional logos and taglines. But their business model depends on you defaulting — because the penalty fees, rollover charges, and harassment tactics are where they extract their real profit.

According to the Federal Competition and Consumer Protection Commission (FCCPC), hundreds of complaints about illegal digital lending practices were filed by Nigerian consumers between 2022 and 2024, leading to the delisting of multiple apps from app stores and the sanctioning of several operators. The numbers continue to grow.

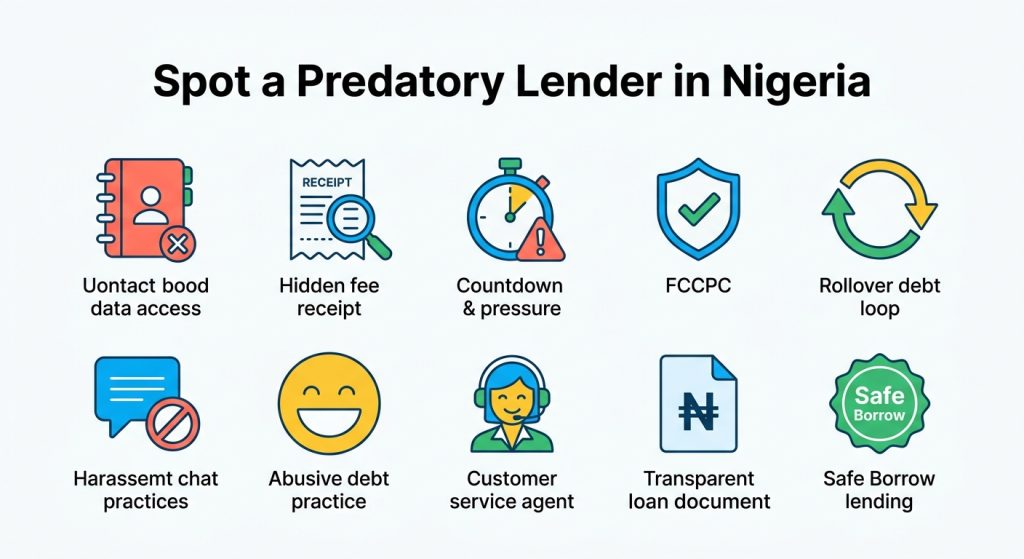

Predatory lending Nigeria cases follow a recognisable pattern. Once you know the nine warning signs below, you will be able to identify a dangerous lender within minutes — before any money changes hands.

Warning Sign #1: They Demand Full Access to Your Contacts, Gallery, and SMS

This is the single biggest red flag in predatory lending Nigeria cases.

A legitimate lender needs your BVN, bank statement, and possibly employment details. That is all.

A predatory app requests permission to read your entire contact list, access your photo gallery, and intercept your SMS messages — buried inside the installation permissions that most people click through without reading.

Why? Because this data is their real collateral. If you miss a payment, they deploy it. They send bulk messages to every contact on your phone — your mother, your boss, your pastor, your classmates — with fabricated or exaggerated claims about your so-called “fraudulent” behaviour.

This practice has been explicitly prohibited by the FCCPC. The Commission’s 2022 Interim Regulation on Digital Lending formally banned apps from accessing borrowers’ device contacts for collection purposes.

What to do: After installing any loan app, check your phone’s permission settings before applying. If the app demands contacts, gallery, or SMS access, delete it immediately. No CBN-approved loan app requires this.

Warning Sign #2: The True Interest Rate Is Hidden Before You Accept

Under the CBN’s Consumer Protection Framework, every licensed lender must disclose the full cost of credit — including the Annual Percentage Rate (APR), all fees, and the total repayment amount — before a borrower confirms a loan.

Predatory apps show a large disbursement figure and a deceptively small daily rate. Here is what that math actually looks like:

Example: A loan app advertises “1% per day.” You borrow ₦20,000 for 30 days.

– Interest = 1% × 30 days = 30%

– Total interest = ₦6,000

– You repay ₦26,000 — before any processing fee or late penalty.

– If they also charge a ₦1,500 “admin fee” upfront, your actual APR exceeds 450% annually.

These are hidden loan charges in Nigeria that borrowers only discover after the money lands in their account — a hallmark of predatory lending in Nigeria.

What to do: Always demand one clear number: What is the total naira amount I repay? Not the daily rate. Not the APR estimate. The total. If the app cannot display this before you confirm, walk away.

Warning Sign #3: They Charge Fees Before the Loan Is Disbursed

You applied for ₦30,000. A message arrives asking you to pay a ₦3,000 “insurance fee” or “verification charge” before the funds are released.

Stop. No legitimate Nigerian lending institution — bank, microfinance bank, or licensed fintech — collects money from you before disbursing your loan. Processing fees, if applicable, are either deducted from the loan amount or added to your repayment schedule. They are never collected upfront.

This tactic is especially common on WhatsApp and Telegram, where illegal loan app operators in Nigeria pose as agents of legitimate fintech brands like Carbon, FairMoney, or Branch to deceive unsuspecting borrowers.

If you pay, the loan never comes. The “agent” disappears. This is one of the fastest-growing forms of predatory lending Nigeria fraud in 2026.

Warning Sign #4: No FCCPC or CBN Registration Is Displayed

The FCCPC maintains a publicly available register of approved digital lenders in Nigeria. The CBN separately licenses microfinance banks and digital moneylenders.

A predatory lender will not display registration credentials — because they frequently operate without them.

What to do: Before borrowing from any app, search the FCCPC’s approved digital lenders list. If the app or company name does not appear there, that is a hard stop. No exceptions.

This single check eliminates the majority of illegal loan apps in Nigeria before you ever expose yourself to them. It is the most time-efficient protection available against predatory lending Nigeria operators.

Warning Sign #5: Repayment Terms Change After You Borrow

You were told 30 days. When the date approaches, the app suddenly claims your agreement was for 14 days. Or the interest charged is higher than what the offer screen displayed.

This happens when terms are buried inside a PDF link nobody reads, written in confusing financial language, or simply altered after disbursement in the backend. Once the money is in your account, some predatory operators treat the original terms as negotiable — on their side only.

What to do: Screenshot the loan offer screen, repayment schedule, and terms summary before you press confirm. Timestamp the screenshots. These images are your legal evidence if a lender tries to retroactively change what you agreed to.

This documentation habit has helped Nigerian borrowers win FCCPC complaints against predatory lenders that attempted to charge undisclosed penalty structures after disbursement.

Warning Sign #6: They Threaten EFCC, Police, or Arrest Over Small Debts

“We have reported you to the EFCC.”

“Our lawyer will file a criminal case against you by Friday.”

“The police will visit your home tomorrow morning.”

These are illegal intimidation tactics. In the vast majority of personal loan cases, they are complete fabrications designed to trigger panic payments.

Here is the legal reality: failing to repay a personal loan in Nigeria is a civil matter, not a criminal offence. You cannot be arrested for owing a loan app ₦15,000. The EFCC investigates financial crimes — fraud and money laundering — not personal loan defaults between a consumer and a lender.

The FCCPC has stated explicitly and repeatedly that threats, public shaming, midnight harassment calls, and bulk messages to a borrower’s contacts are illegal debt collection practices under Nigerian consumer protection law. Every one of these messages is reportable and actionable. This is predatory lending Nigeria behaviour at its most aggressive — and it is illegal.

Warning Sign #7: No Physical Address, Working Support Line, or Complaint Channel

Real lenders want you to reach them when there is a problem — because real lenders carry accountability.

A predatory lending operation in Nigeria has no working phone number, no verified office address, and no live customer support. The only messages you receive are automated repayment demands or, once you are late, escalating threats.

What to do: Test customer service before you borrow. Send a message. Try the support line. If you cannot reach a human being at a company before you give them your BVN, you will not reach one when your salary is delayed and you need to negotiate. That asymmetry is intentional and is one of the defining traits of predatory lending Nigeria platforms.

Warning Sign #8: Rollover Loans That Reset Your Debt Every Cycle

You cannot repay this month. The app offers a “rollover” — extend the loan for 30 more days, but first pay a rollover fee of ₦4,000.

You pay the fee. Your principal does not reduce by one naira. Thirty days later, you are in exactly the same position, now ₦4,000 poorer.

This is a textbook debt trap in Nigeria. Some borrowers have documented paying two to three times their original loan amount in rollover and penalty fees — while the principal balance remains completely untouched.

Example: You borrowed ₦25,000. You roll over three times at ₦5,000 per rollover. You have paid ₦15,000 in fees. You still owe ₦25,000. Total cost so far: ₦40,000 — with the debt unresolved.

What to do: If you genuinely cannot repay, contact the lender before the due date to negotiate a restructured payment plan. A legitimate lender will negotiate. A predatory one offers only the rollover. That difference tells you everything about who you borrowed from.

Warning Sign #9: Countdown Timers and Urgency Pressure to Force Fast Acceptance

“You have been pre-approved! This offer expires in 00:09:47.”

The countdown timer is a psychological manipulation tool. Its only function is to prevent you from reading the terms, running the math, or asking someone you trust for advice. Legitimate lenders do not use this tactic — because credit decisions are based on your financial profile, not a manufactured clock.

If a lender is using extreme urgency to push you past your own judgment, they are not operating in your interest. Every reputable Nigerian fintech allows you to review a loan offer at your own pace before confirming. Countdown pressure is a clear hallmark of predatory lending in Nigeria — and reason enough to close the app permanently.

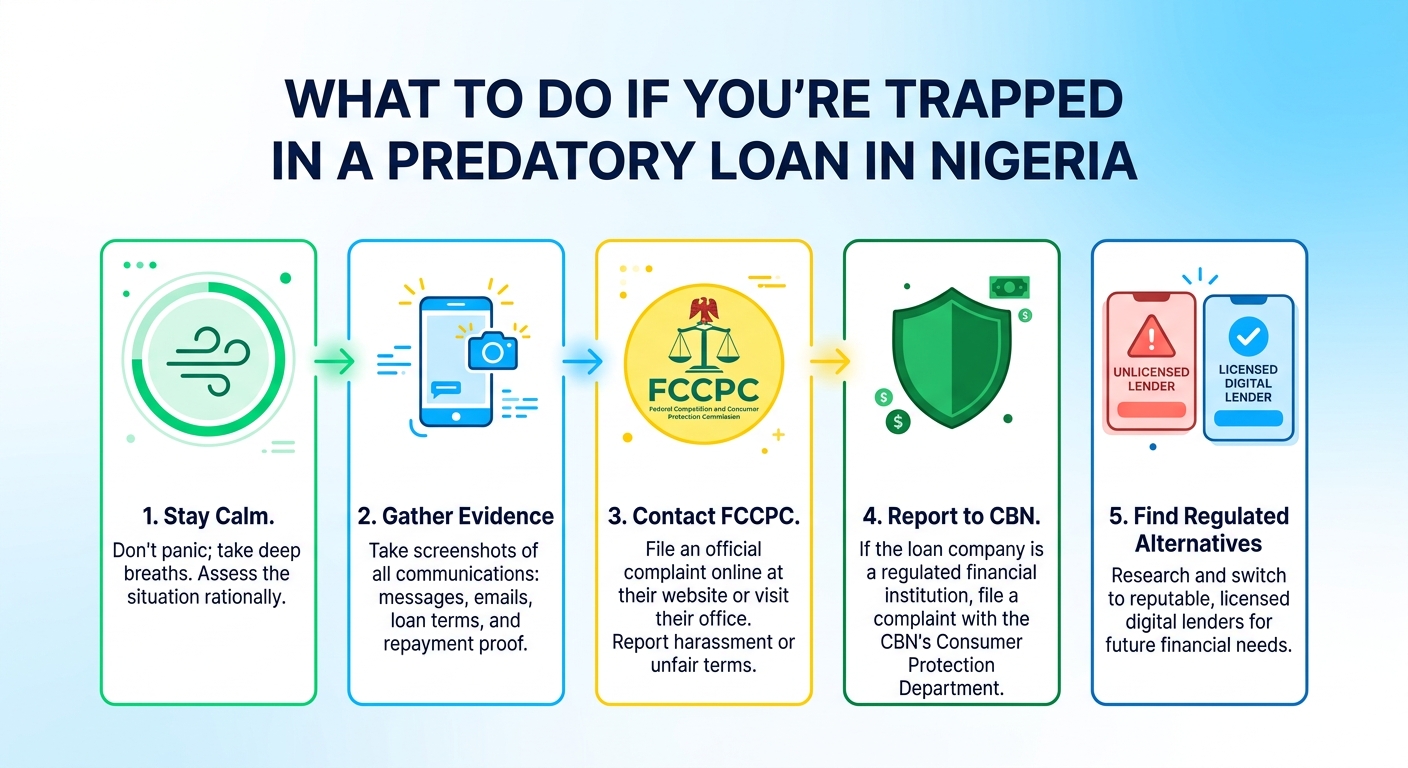

You Are Already Inside a Predatory Loan. What Do You Do Right Now?

If predatory lending in Nigeria has already caught you, here are the exact steps to take — in order.

Step 1 — Stop panicking. Harassment messages are engineered to make you act before you think. They cannot jail you for a personal loan default. Take a breath before you do anything else.

Step 2 — Document everything. Screenshot every threatening message, every call log, every message sent to your contacts. Date-stamp them. These are your legal evidence.

Step 3 — Report to the FCCPC. File a formal complaint at fccpc.gov.ng or contact their consumer protection line. The FCCPC has sanctioned multiple loan apps, removed them from app stores, and has the authority to pursue enforcement action on your behalf.

Step 4 — Report to the CBN. If the lender claims CBN licensing but is engaging in illegal collection behaviour, file a complaint with the CBN Consumer Protection Department at consumerprotection@cbn.gov.ng. The CBN takes licence violations seriously.

Step 5 — Seek legitimate refinancing. If the debt is real and you genuinely owe it, look for a CBN-approved loan app or FCCPC-listed lender who can help you consolidate at legal interest rates and transparent terms. Refinancing out of a predatory loan into a legitimate one is a valid and often smart financial strategy. You can compare verified options at SmartLoans.ng.

The Pre-Borrow Checklist: Safe Lender vs. Predatory Lender

| Check | Safe Lender | Predatory Lender |

|---|---|---|

| FCCPC approved list | ✅ Listed | ❌ Not listed |

| Shows total ₦ repayment before confirmation | ✅ Always | ❌ Hides full cost |

| Demands contacts/gallery/SMS access | ❌ Never requests | ✅ Demands it |

| Physical address and working support line | ✅ Available | ❌ Absent |

| No upfront fee before loan arrives | ✅ Correct | ❌ Charges pre-payment |

| Uses countdown pressure to force acceptance | ❌ Never | ✅ Standard tactic |

| Threatens EFCC/police over small debts | ❌ Never | ✅ Routine intimidation |

Save this checklist. Run any lender against it before you borrow — and share it with anyone who is considering a loan app for the first time.

Frequently Asked Questions

Can a loan app in Nigeria actually have me arrested?

No. Defaulting on a personal loan is a civil matter in Nigeria. A lender can pursue you through civil court for an outstanding amount — but they cannot initiate a criminal arrest. Any threat of EFCC involvement or police action over a personal loan default is an illegal intimidation tactic and a defining trait of predatory lending Nigeria operators.

How do I check if a loan app is FCCPC-approved?

Visit fccpc.gov.ng and search their register of approved digital lenders. The list is publicly accessible and updated periodically. Any app not on this list should be avoided entirely.

What is the maximum legal interest rate for loan apps in Nigeria?

The CBN requires full transparency on credit pricing, but there is no single fixed cap for all digital lenders. The FCCPC has, however, flagged effective annual rates exceeding 400% as exploitative in several enforcement actions taken against predatory lending operators.

What if a predatory lender has already messaged my contacts?

Document every message sent. File a complaint with the FCCPC immediately. The FCCPC’s 2022 interim regulation explicitly prohibits this practice, and enforcement actions have resulted in app delisting and fines for operators who use contact list harassment as a collection tool.

Final Word: Desperation Is Not a Reason to Ignore Red Flags

The cruelest design feature of predatory lending in Nigeria is that it targets people at their most vulnerable — when rent is overdue, when a child is sick, when the salary has not arrived but the responsibilities have.

Predatory lenders understand this perfectly. They build their products to catch you in exactly that moment, when your risk judgment is compromised by stress and urgency.

The most powerful protection is preparation. Learn the warning signs before you are desperate. Know your rights under FCCPC regulation before a lender tests them against you. And when you do need to borrow, choose a lender who is on the FCCPC-approved list, shows you the full repayment cost upfront, and has earned your trust before asking for access to your financial life.

That is what safe borrowing in Nigeria looks like — and it is available to you right now if you know where to look.

SmartLoans.ng connects Nigerian borrowers with CBN-compliant, FCCPC-listed lenders who are transparent about their rates, do not access your contacts, and provide real customer support. Visit SmartLoans.ng to compare verified loan options safely.