The loan app says you qualify for ₦150,000. But should you collect all of it?

Most Nigerians never stop to ask that question. They see the approved amount, they collect it — and three weeks later, repayment has swallowed half their salary and the month has collapsed.

This is not a loan app problem. This is a borrowing limit problem — and it has a name: your debt-to-income ratio Nigeria lenders use internally but almost never show you.

Understanding your debt-to-income ratio in Nigeria before you borrow could be the difference between a loan that solves your problem and a loan that becomes your new problem. This guide breaks it down in plain Naira-and-kobo language, with real examples from real Nigerian situations — so you can set your own safe borrowing limit before you sign anything.

What Debt-to-Income Ratio Actually Means (Plain English)

Your debt-to-income ratio is a simple comparison between how much you owe every month and how much you earn every month.

Think of it this way:

If your salary is ₦100,000 and you’re already spending ₦40,000 on loan repayments, rent installments, and other fixed obligations — then 40% of your income is already gone before it arrives.

That percentage is your DTI. The lower it is, the more financial breathing room you have. The higher it is, the closer you are to a debt spiral — where you borrow new money just to repay old debt.

This is not a theoretical concept. The Central Bank of Nigeria (CBN), in its consumer credit framework, recommends that total debt service — meaning all monthly loan repayments combined — should not exceed 30–33% of net monthly income. Some lenders use 40% as their hard ceiling, but anything above that threshold is considered high-risk territory for the borrower.

Nigerian loan apps rarely show you this calculation. They show you what you qualify for — not what you can safely repay. Those are two entirely different numbers, and confusing them is how most borrowers end up in trouble.

How to Calculate Your Own DTI in 3 Steps (With ₦ Examples)

You do not need a spreadsheet or a finance degree. You need your phone calculator and honest numbers.

Step 1: Add Up All Monthly Debt Obligations

Include every committed payment that leaves your account:

- Active loan repayments (loan apps, bank loans, cooperative loans)

- Monthly rent or rent installments

- Buy Now Pay Later (BNPL) repayments

- Regular family remittances that are non-negotiable

- Any other fixed monthly financial obligations

Example — Chioma, a civil servant in Enugu:

– Loan app repayment: ₦18,000/month

– Rent contribution (annual rent ÷ 12): ₦12,500/month

– Cooperative contribution: ₦5,000/month

– Total monthly obligations: ₦35,500

Step 2: Establish Your Net Monthly Income

Net income = what actually lands in your account after tax, pension, and NHIS deductions. Not your gross salary. Not the figure on your offer letter.

- Chioma’s net monthly salary: ₦95,000

Step 3: Apply the DTI Formula

DTI = (Total Monthly Obligations ÷ Net Monthly Income) × 100

Chioma’s DTI = (₦35,500 ÷ ₦95,000) × 100 = 37.4%

She is in the caution zone. If she takes another loan without first reducing an existing obligation, she risks crossing into high-risk territory — and that is precisely where monthly shortfalls and missed repayments begin.

This three-step process is the core of understanding debt-to-income ratio Nigeria borrowers should apply before any new credit decision.

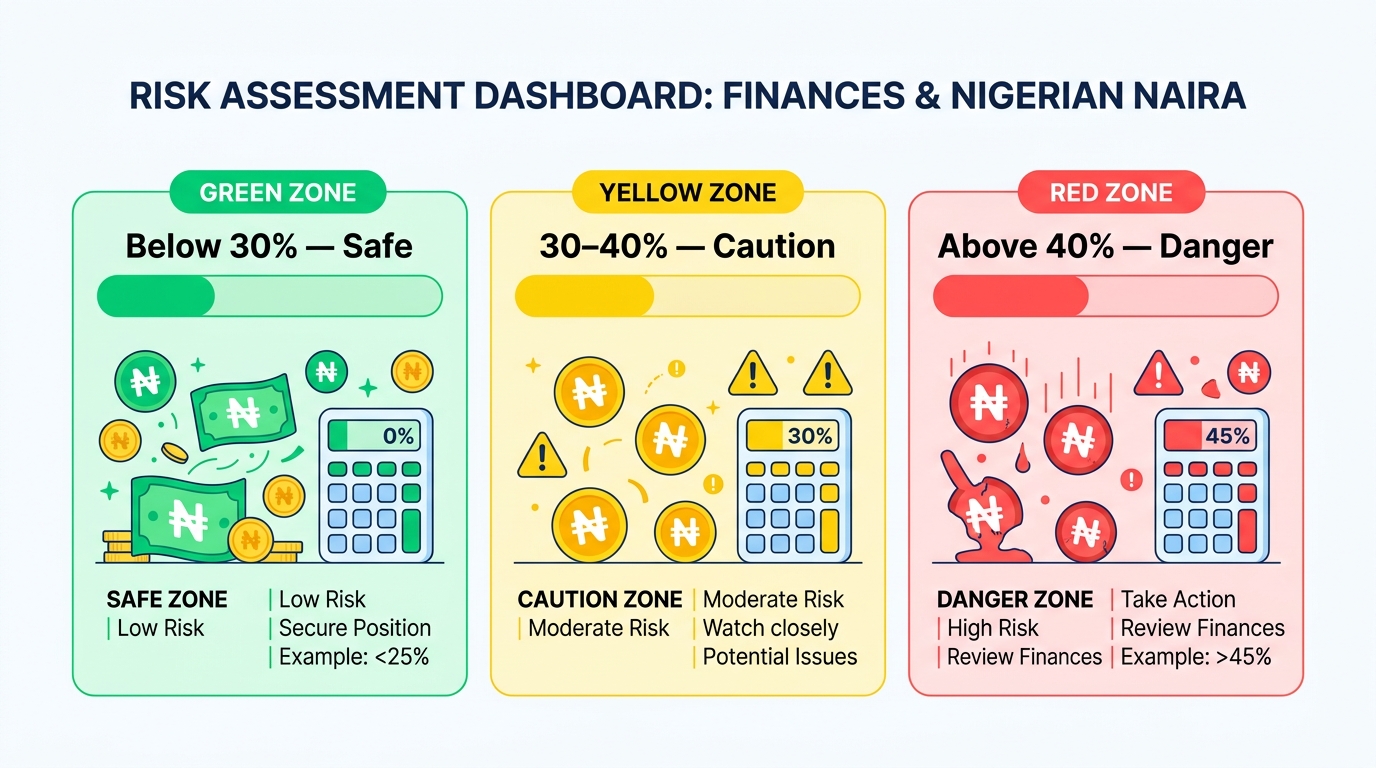

What the Numbers Mean: Safe, Caution, and Danger Zones

Calculating your debt-to-income ratio Nigeria figure is only half the work. Reading the result correctly is what shapes your decision.

| DTI Range | What It Means | Recommended Action |

|---|---|---|

| Below 30% | Safe zone — healthy financial headroom | You can consider a loan if the need is genuine |

| 30–40% | Caution zone — manageable but tight | Borrow the minimum needed, not the full approved amount |

| 40–50% | High-risk zone — financially stretched | Only borrow for genuine emergencies; repay aggressively |

| Above 50% | Danger zone — debt spiral risk is real | Pause new borrowing entirely; reduce existing debt first |

These thresholds align with guidance from the Federal Competition and Consumer Protection Commission (FCCPC), which oversees digital lenders in Nigeria and has issued directives requiring lending apps to consider borrower affordability — not just repayment probability — before disbursing funds. See FCCPC’s regulatory guidelines on digital lenders.

If your DTI is already at 52% and a loan app is offering you ₦200,000, that is not generosity. That is a revenue decision. The app is not measuring your financial safety — it is measuring its own risk of default, which is a very different calculation.

Why Nigerian Loan Apps Don’t Show You This Number

Here is an uncomfortable truth about how most digital lending in Nigeria works.

Loan apps are incentivized to lend more, not less. Their revenue comes from interest, processing fees, and rollover penalties. A borrower who collects a larger amount pays more fees. The approval algorithm is designed to assess the app’s risk of non-repayment — not your risk of financial hardship.

There is a meaningful difference between those two outcomes.

An app can determine that you will likely repay — because your BVN, transaction history, and bank statement suggest stable income — without accounting for the fact that repaying leaves you with ₦6,000 for groceries for the rest of the month.

According to EFInA’s Access to Finance survey data, over 40% of Nigerian adults who use credit report experiencing repayment difficulty at some point. This is not primarily a willpower problem. It is largely a borrowing-more-than-your-income-can-carry problem — which is exactly what your debt-to-income ratio Nigeria calculation is designed to prevent. EFInA Nigeria Financial Access Data.

Knowing your own DTI before applying puts you in control, regardless of what any app tells you that you qualify for.

Real-Life Examples: Lagos Salary Earner, Abuja Corper, Keke Rider

Example 1 — Tunde, Keke Rider in Lagos

- Average daily income: ₦5,500 | Monthly (after fuel and maintenance set-aside): ~₦110,000

- Existing loan repayment: ₦15,000/month

- Current DTI: 13.6% ✅ Safe zone

His bike needs a ₦35,000 repair. He is evaluating a 3-month loan with roughly ₦13,500/month repayment.

New DTI = (₦15,000 + ₦13,500) ÷ ₦110,000 = 25.9% ✅ Still safely within the safe zone. This is a productive loan — it protects his primary income source without straining his cash flow.

Example 2 — Amaka, NYSC Corper in Abuja

- Monthly allawee + part-time tutoring income: ₦55,000

- Shared accommodation contribution: ₦10,000/month

- No existing loans

- Current DTI: 18.2%

She wants ₦80,000 for a laptop to support her tech training. A 6-month repayment plan equals approximately ₦15,000/month.

New DTI = (₦10,000 + ₦15,000) ÷ ₦55,000 = 45.5% ⚠️ High-risk zone.

Better approach: Borrow ₦40,000 instead. Monthly repayment drops to ~₦7,500.

Revised DTI = (₦10,000 + ₦7,500) ÷ ₦55,000 = 31.8% — caution zone, but workable. She gets the laptop, starts building income, and revisits a top-up loan after her financial position strengthens.

Example 3 — Babatunde, Factory Worker in Ogun State

- Net monthly salary: ₦72,000

- Current obligations: Two loan app repayments (₦20,000 + ₦8,000) + cooperative (₦5,000) + family remittance (₦5,000) = ₦38,000/month

- Current DTI: 52.8% ❌ Danger zone

He wants to borrow ₦60,000 for his daughter’s school fees. Any new loan repayment would push his DTI above 65%.

He will almost certainly default or be forced into a debt cycle — borrowing a third loan to service the first two.

Better path for Babatunde:

1. Negotiate a split-payment plan directly with the school

2. Request a salary advance from his employer (zero or near-zero cost)

3. Clear one existing loan app debt first before adding new obligations

4. Borrow only the remaining balance once DTI drops below 40%

This is not about being unable to provide for his daughter. It is about sequencing correctly so the loan does not destroy his ability to provide consistently over the months ahead.

These three examples show how the debt-to-income ratio Nigeria framework applies differently across income levels and life situations — the formula is the same, but the right decision changes based on the numbers.

How DTI Affects Your Loan Approval Chances in Nigeria

Lenders who operate responsibly — and those aligned with CBN consumer credit guidelines — use versions of DTI assessment during underwriting. Here is what happens behind the scenes when you apply:

- Bank statement analysis identifies existing debit mandates and recurring loan repayment patterns

- BVN cross-referencing surfaces loans held across multiple lenders simultaneously

- Credit bureau checks via CRC Credit Bureau or FirstCentral reveal outstanding balances and repayment history

- Salary or income verification establishes the income baseline for the affordability ratio calculation

If your DTI signals over-indebtedness, a responsible lender will reduce your approved amount or decline the application entirely. If a lender approves you despite an obviously dangerous debt-to-income ratio Nigeria calculation — that is a warning about that lender’s practices, not a green light for you to proceed.

Knowing your own DTI before you apply means you will not be blindsided by a reduced offer, and more importantly, you will not be tempted to accept a full approval that already exceeds your safe borrowing limit.

5 Signs You’re About to Borrow More Than You Can Repay

Watch for these warning signals before you confirm any loan:

- The monthly repayment alone exceeds 30% of your take-home pay — before counting any other obligation you already carry

- You’re borrowing to repay another loan — this is debt cycling, and it compounds faster than most people expect

- You can’t name what you’ll cut from your budget to fund repayment — a vague plan is not a plan

- You’re choosing the longest repayment term to make it “feel” affordable — longer terms reduce monthly pain but significantly increase total cost

- You’ve already missed a repayment this year — your debt-to-income ratio Nigeria position is likely already strained; adding new debt worsens it without resolving the underlying squeeze

If two or more of these apply to your situation right now, stop before confirming. Step back, recalculate your DTI, and make a decision based on your actual numbers — not the approval screen.

What to Do If Your Debt-to-Income Ratio Is Already Too High

If the calculation reveals you are already in caution or danger territory, here is a practical sequence to follow:

1. Stop adding new debt immediately. Pause all loan applications, including “small” ones. Small repayments stack. A ₦4,000/month obligation added to a ₦38,000/month load is not small — it is another weight on a structure that is already under strain.

2. List every obligation with its exact repayment date. Visibility precedes control. A phone note or paper list works. What you can see clearly, you can manage strategically.

3. Contact existing lenders before you miss payments. Many licensed Nigerian digital lenders have restructuring options for borrowers who reach out proactively. Once you default and penalties begin accruing, your options shrink rapidly and your debt-to-income ratio Nigeria position deteriorates further.

4. Apply the debt snowball method. Identify your smallest active loan. Direct any freed-up cash toward clearing it first. Once it is cleared, redirect that repayment amount toward the next smallest debt. This method builds momentum and improves your DTI faster than paying minimum amounts across all debts simultaneously.

5. Explore zero-cost alternatives before borrowing again. Salary advance from employer, cooperative emergency funds, family support, or selling an underused asset. These options do not add to your external debt load and do not carry the compounding costs that loan apps charge.

6. Set a DTI target before your next loan application. Commit to not borrowing again until your ratio drops below 35%. This gives you a concrete, measurable goal rather than a vague intention to “be more careful next time.”

Borrow Within Your Safe Limit with LendSafe

Once you have calculated your debt-to-income ratio Nigeria figure and identified your actual safe borrowing window, the next step is finding a lender whose process works with that reality rather than against it.

At LendSafe, the approach is built around responsible borrowing. Rather than simply showing you the maximum amount you qualify for, the platform is designed to help you understand what you can comfortably repay based on your income and existing obligations. You see a recommended borrowing range — not just a ceiling figure engineered to maximize what you collect.

Transparent repayment terms, clear total cost of credit, and an affordability-first approach make it a practical starting point if you want to borrow without compromising your monthly stability.

The goal is straightforward: you borrow, you solve your problem, and you repay without destroying the rest of your month.

The One Number Every Nigerian Borrower Should Calculate First

Before you take any loan in Nigeria — from an app, a bank, a cooperative, or anywhere else — calculate your debt-to-income ratio.

It takes five minutes. Add up your monthly obligations. Write down your net income. Divide and multiply by 100.

- Below 30%: You have room. Borrow responsibly if the need is genuine.

- 30–40%: Borrow carefully. Take less than your maximum approval.

- 40–50%: Danger is close. Only borrow for true emergencies.

- Above 50%: Stop. Clear existing debt first. Protect what remains.

The loan app will always show you more than you should collect. The interest rate advertisement will always make repayment look manageable. Your job — armed with your own debt-to-income ratio Nigeria calculation — is to collect only what your income can actually carry without breaking your monthly budget.

That one honest calculation, done before you sign anything, could save you months of financial pain and the kind of debt spiral that takes years to fully exit.

All ₦ figures used in this article are illustrative examples based on typical Nigerian income and borrowing scenarios. Actual loan amounts, interest rates, and repayment terms vary by lender and individual financial assessment. Always verify terms directly with your chosen lender before signing.