How to Improve Your Credit Score in Nigeria: A Step-by-Step Guide

So, you’ve checked your credit score and the number wasn’t what you hoped for. Don’t panic. The journey to improve your credit score in Nigeria is not just possible—it’s a clear path you can start on today. A credit score isn’t a permanent label; it’s a dynamic snapshot of your financial health, and you have the power to change it.

Improving your credit score is one of the most impactful financial moves you can make. It’s the key that unlocks better loan offers, lower interest rates, and greater financial freedom. This guide will provide a step-by-step plan to take control and build a score that makes lenders say ‘yes.’

Why a Good Credit Score is Your Financial Superpower in Nigeria

Think of your credit score as your financial reputation. In Nigeria’s growing credit economy, this reputation is everything. Lenders, from major commercial banks to popular fintech loan apps, use this three-digit number to quickly assess the risk of lending you money.

A strong credit score translates into tangible benefits:

* Higher Loan Approval Rates: You’re more likely to be approved for personal loans, car financing, or mortgages.

* Lower Interest Rates: Lenders see you as a reliable borrower, rewarding you with more favourable interest rates that save you thousands of Naira over the life of a loan.

* Increased Borrowing Power: A good score can grant you access to larger loan amounts.

* Faster Loan Processing: With a proven track record, loan applications are often processed much quicker.

Simply put, a good credit score gives you options and bargaining power. It’s a critical tool for achieving your financial goals.

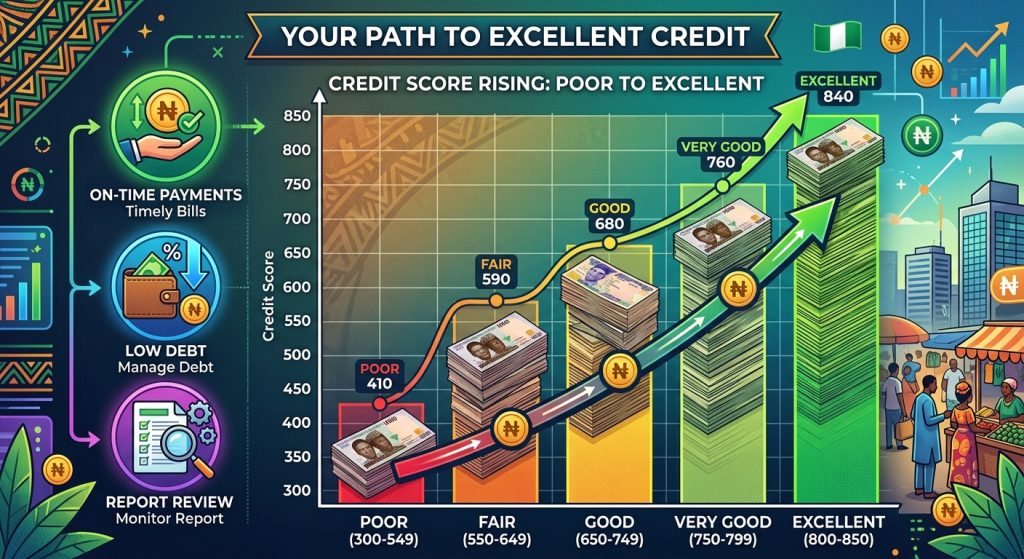

Understanding the “Good” Credit Score Range in Nigeria

Before you can improve your score, you need a target. In Nigeria, credit scores are managed by licensed credit bureaus like CRC Credit Bureau and FirstCentral Credit Bureau. While their exact models may differ slightly, they generally follow a similar range:

- Excellent: 800 – 850

- Very Good: 740 – 799

- Good: 670 – 739

- Fair: 580 – 669

- Poor: 300 – 579

If your score is in the “Fair” or “Poor” range, that’s where we’ll focus our efforts. The goal is to consistently climb into the “Good” range and beyond.

The 5 Pillars That Determine Your Nigerian Credit Score

Your score isn’t random; it’s calculated based on specific data in your credit report. Understanding these five pillars is crucial to knowing which levers to pull.

- Payment History (35%): This is the single most important factor. Do you pay your debts on time? Late payments, defaults, and collections severely damage your score.

- Credit Utilisation (30%): This measures how much of your available credit you’re using. If you have a credit card or a digital credit line with a ₦100,000 limit and you’ve used ₦80,000, your utilisation is 80%—which is very high.

- Length of Credit History (15%): How long have you been using credit? A longer history of responsible borrowing demonstrates stability and is viewed positively.

- New Credit (10%): How often are you applying for new loans or credit lines? Applying for too much credit in a short period can be a red flag.

- Credit Mix (10%): Do you have a healthy mix of different types of credit? This could include installment loans (like a personal loan) and revolving credit (like a credit line from Carbon or a bank).

Now, let’s turn this knowledge into an actionable plan.

Step 1: Master Your Payment History (The #1 Factor)

If you do only one thing, let it be this: Pay every single bill on time. A single late payment can stay on your credit report for years.

Actionable Steps:

* Automate Your Payments: Set up automatic debits or transfers from your salary account for loan repayments and utility bills. This is the most effective way to avoid forgetting.

* Set Up Reminders: Use your phone’s calendar or a budgeting app to set reminders a few days before each due date.

* Address Past-Due Accounts: If you have any accounts in default, contact the lender immediately. Negotiate a payment plan to bring the account current. It’s better to start paying something than to continue ignoring it.

Step 2: Control Your Credit Utilisation Ratio (CUR)

This is the second most powerful tool in your arsenal. Lenders get nervous when they see you’re using most of your available credit, as it suggests you might be overstretched. The golden rule is to keep your CUR below 30%. According to Investopedia, a lower ratio is always better.

How to Calculate It:

CUR = (Total Amount You Owe) / (Your Total Credit Limit)

Example: You have a ₦50,000 credit line from a fintech app and owe ₦10,000. Your CUR is ₦10,000 / ₦50,000 = 20%. This is great!

Actionable Steps:

* Pay Down Balances: Focus on paying down the balances on your revolving credit lines.

* Make Multiple Payments: You don’t have to wait for the due date. Making a payment mid-month can help keep your reported balance low.

Step 3: Build a Long and Healthy Credit History

Lenders love stability. A long credit history gives them more data to see that you’re a consistent and reliable borrower.

Actionable Steps:

* Don’t Close Old Accounts: It can be tempting to close an old, unused credit account. Resist this urge. That account, even with a zero balance, contributes positively to the average age of your credit history. Keeping it open (and in good standing) helps your score.

* Start Early: The sooner you start building credit responsibly, the better.

Step 4: Be Strategic About New Credit Applications

Every time you apply for a new loan or credit line, it results in a “hard inquiry” on your credit report. While one or two inquiries won’t hurt much, a flurry of applications in a short time makes you look desperate for credit, which is a major red flag for lenders.

Actionable Steps:

* Apply Only When Necessary: Don’t apply for credit on a whim.

* Space Out Applications: If you need to apply for multiple lines of credit, try to space them out by at least six months.

* Check Eligibility First: Many lenders offer pre-qualification tools that don’t impact your score. Use these to gauge your chances before submitting a formal application.

How to Build Credit from Scratch in Nigeria (For Beginners)

What if you have no credit history (a “thin file”)? You need to give the credit bureaus something to report.

- Start Small: Apply for a small, manageable loan from a reputable digital lender that reports to the credit bureaus (like Carbon, FairMoney, or Branch). You can compare options for these small loans to find one that suits you. Start with an amount you can comfortably repay on time.

- Get a Secured Credit Card: Some banks offer secured credit cards where you provide a cash deposit as collateral. Use it for small purchases and pay the bill in full every month.

- Become an Authorized User: If you have a trusted family member with excellent credit, ask them to add you as an authorized user on one of their credit cards. Their good payment history can reflect positively on your report.

Common Nigerian Mistakes That Crush Your Credit Score

- Defaulting on a Fintech “Quick Loan”: Many people mistakenly believe these small digital loans don’t matter. They do. Most reputable fintechs report defaults to the major credit bureaus like FirstCentral.

- Ignoring Utility Bills: While not always reported, an increasing number of service providers are beginning to report payment data. Always pay your electricity (NEPA/PHCN), DSTV, and other bills on time.

- Being a Guarantor for an Unreliable Friend: When you stand as a guarantor, their debt becomes your legal responsibility. If they default, it’s your credit score that gets destroyed. Be extremely cautious about who you guarantee a loan for.

Your Roadmap to a Better Score: Patience is Key

Improving your credit score is a marathon, not a sprint. You won’t see a 200-point jump overnight. The negative information on your report will take time to age, while your new positive habits will take a few months to reflect meaningfully.

By following these steps—paying on time, keeping balances low, and being strategic with new credit—you are building a powerful foundation for your financial future. Stay disciplined, be patient, and watch as your financial reputation grows, opening doors to opportunities you never thought possible.